Quick Answer: AI Agents For Loan Processing

AI agents for loan processing are supervised software workflows that help lending teams collect borrower information, check document completeness, retrieve policy context, prepare underwriting summaries, route exceptions, and maintain review evidence. They should support loan operations, not replace licensed judgment, credit policy, compliance review, or final approval.

The strongest starting point is a narrow loan workflow where the agent can prepare work for a human team: borrower intake, document checklisting, KYC support, policy Q&A, risk flag summaries, or exception queue triage. If the workflow needs access to core lending systems, document stores, credit data, CRM records, or case-management tools, treat it as a production AI system with identity, permissions, audit logs, evaluations, and rollback paths. NextPage's AI development services focus on that practical layer: workflow mapping, secure integrations, retrieval design, human review, and measurable rollout.

Where AI Agents Fit In Loan Processing

Loan processing is full of repeatable coordination work: collecting borrower information, matching documents to requirements, checking whether a file is ready for review, summarizing evidence, asking follow-up questions, and moving cases between intake, underwriting, compliance, and servicing teams. AI agents are useful when that coordination work depends on context from multiple systems and when every output can be reviewed. Teams planning bank-grade lending workflows can also compare this operating model with NextPage's AI agents for banking and finance workflows, especially the loan intake and document review patterns.

A practical loan-processing agent does not decide whether someone should receive credit. It helps the team understand the file faster. It can identify missing documents, summarize income evidence, compare a file against checklist rules, retrieve relevant policy snippets, draft an underwriter note, or route a case to a specialist queue. This makes it closer to AI workflow automation than a black-box decision engine.

The architecture should make boundaries explicit. What can the agent read? What can it write? Which actions are draft-only? Which outcomes require a human underwriter, compliance reviewer, or operations lead? Those boundaries are the difference between a helpful workflow assistant and an uncontrolled system that creates operational and regulatory risk.

Loan Processing Use Cases

Good use cases are high-volume, document-heavy, and easy to audit. They save time without handing the agent final lending authority. The table below shows where AI agents usually fit best in a first lending workflow pilot.

| Workflow | Agent can help with | Human review point |

|---|---|---|

| Borrower intake | Classify request type, collect missing fields, summarize applicant-provided context, and create the case record | Confirm data quality, consent, eligibility boundaries, and next step |

| Document checklisting | Match uploaded files to required document types, flag gaps, extract key fields, and prepare follow-up requests | Validate extraction, handle ambiguous documents, and approve borrower communication |

| KYC and AML support | Organize identity, business, ownership, sanctions-screening, and risk-review evidence for internal workflows | Compliance team confirms requirements, exceptions, and escalation decisions |

| Policy retrieval | Find relevant policy excerpts, product rules, exception criteria, and underwriting guidance from approved sources | Underwriter interprets policy and applies institution-specific judgment |

| Underwriting support | Summarize income, liabilities, collateral notes, risk flags, and file history for review | Underwriter makes the recommendation or decision under approved policy |

| Exception routing | Send cases to underwriting, compliance, fraud, legal, or operations queues based on defined signals | Specialist reviews edge cases and documents the final decision |

Before choosing a use case, estimate the operational value. The AI Automation ROI Calculator can help compare manual hours, case volume, complexity, and expected payback for different loan operations workflows.

Intake And Document Checklisting

Borrower intake is often the safest place to start because it is repetitive and measurable. A supervised agent can read an application package, identify the loan type, check whether required fields are present, detect missing documents, and prepare a concise intake summary. It can also draft a follow-up message for missing information, but the final communication should be reviewed if it affects eligibility, timeline, fees, or sensitive borrower data.

Document checklisting is another strong candidate. Instead of asking operations staff to manually open every upload, an agent can classify file types, extract basic fields, compare the file set against product requirements, and mark each item as present, missing, unclear, expired, or requiring specialist review. The agent should always show the evidence behind each status so the reviewer can verify the source page, field, date, or document version.

This workflow usually needs document AI, OCR, validation rules, and case-management integration. If the file types are inconsistent or scanned documents are low quality, pilot scope should include data cleanup and exception handling. The goal is not perfect automation on day one; it is fewer incomplete files reaching underwriting.

KYC, AML, And Compliance Support

KYC and AML workflows are high-risk areas, so the agent should support evidence organization and review routing rather than decide compliance outcomes. It can prepare identity check summaries, collect business ownership documents, flag missing beneficial-owner information, route high-risk cases, and keep an audit trail of what was reviewed. The rules, thresholds, data sources, and escalation paths must be approved by the institution's compliance team and legal counsel. Teams that need a broader bank compliance workflow view can compare this operating model with NextPage's AI compliance automation for banks guide, which focuses on KYC, AML, audit trails, and human review.

For banking and fintech teams, this is where secure architecture matters. An agent may need access to sensitive borrower data, third-party screening outputs, internal policies, and case notes. Permission scopes, field-level access, retention rules, and logs should be designed before implementation. The security principles in NextPage's secure AI agent development checklist are especially relevant: define the agent charter, limit tools, require approval gates, and record every sensitive action.

The article should not be read as compliance advice. Regulations and supervisory expectations vary by market, institution, product type, and customer profile. Treat the agent as a way to make compliance workflows more organized and auditable, not as a substitute for regulated review.

Policy Retrieval And RAG

Many lending teams already have the information needed to process a file, but it is scattered across product guides, exception policies, underwriting manuals, servicing notes, credit policy documents, and internal knowledge bases. A retrieval-augmented generation workflow can help an agent answer operational questions from approved sources and cite the policy snippets used in the summary.

For example, the agent might retrieve product-specific document requirements, debt-to-income exception rules, collateral review guidance, or escalation criteria. It should not invent policy. It should show the retrieved source, document version, date, and confidence signal so the reviewer can decide whether the guidance applies. This is the practical lane for LLM development in loan operations: grounded retrieval, controlled summaries, evaluations, and integration with the team's workflow tools.

Version control is important. If a policy changes, the agent's retrieval index and evaluation set must change too. A stale policy answer can be worse than no answer because it gives the reviewer false confidence. Build a refresh process, owner, and test set before expanding the system to more products.

Underwriting Support With Human Review

Underwriting support is valuable but should be introduced carefully. A supervised agent can summarize the file, list verified documents, extract borrower-stated facts, highlight risk flags, show policy references, and prepare questions for the underwriter. It can reduce review preparation time, but the underwriter still needs to apply approved credit policy and institution-specific judgment.

Good underwriting summaries separate facts, extracted data, assumptions, missing evidence, and agent-generated interpretation. This distinction matters because reviewers need to know what the source documents say versus what the agent inferred. The summary should also show unresolved issues, such as missing statements, inconsistent employer names, unusual transaction patterns, document quality problems, or manual override requests.

If the organization is deciding whether to build this as a custom workflow, compare the operational complexity against broader software scope. NextPage's custom software development work often starts by mapping roles, data flows, permissions, integration points, and reporting needs before selecting the AI layer. Loan operations agents are no different: the workflow design decides whether the model output is useful.

Exception Routing And Audit Trails

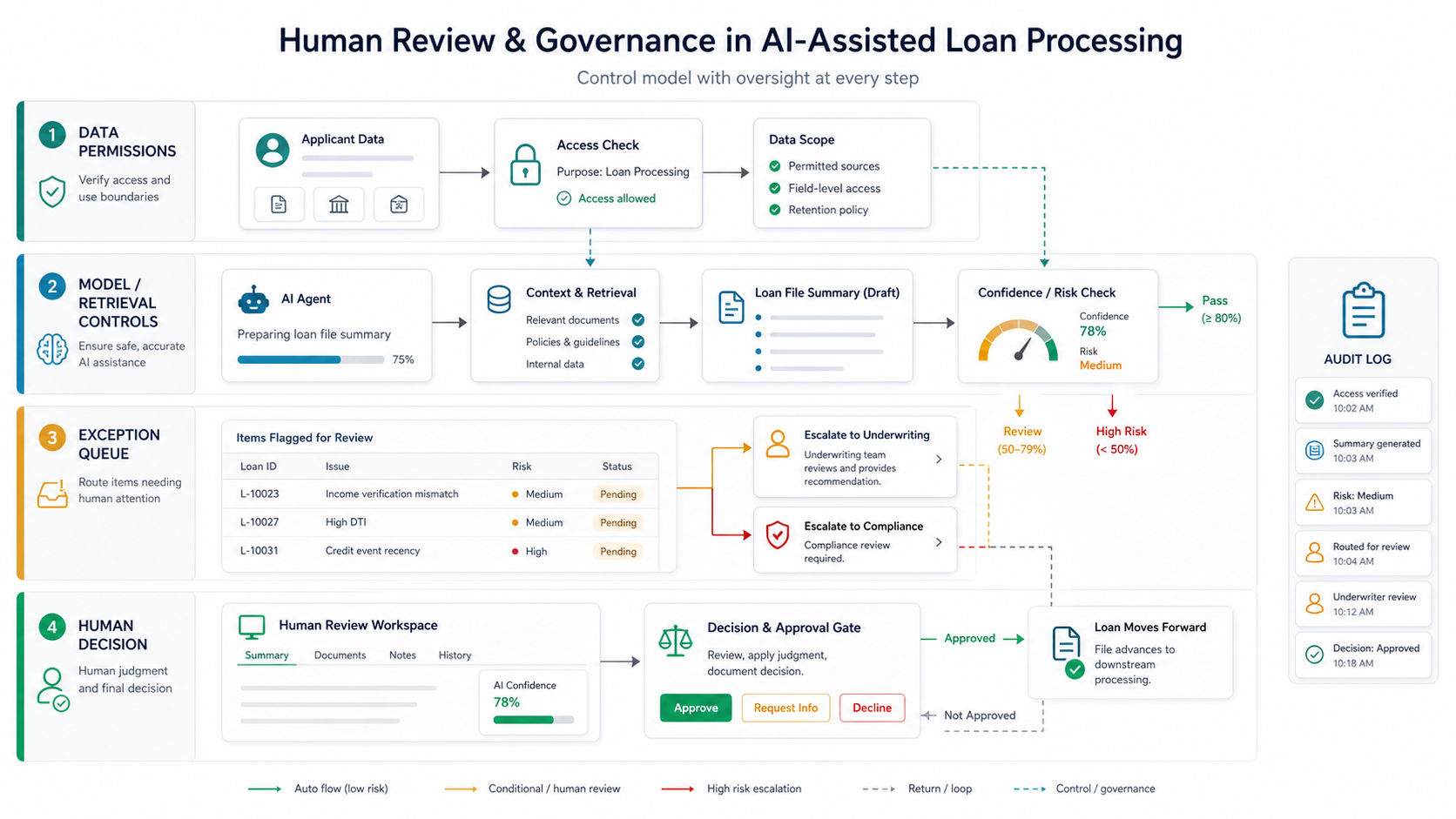

Exception routing is often the point where AI agents produce the clearest operational value. A loan file may need underwriting review, compliance review, fraud review, missing-document follow-up, income verification, appraisal follow-up, or borrower clarification. An agent can classify the exception, attach the supporting evidence, recommend the next queue, and create a task for the right team.

Every route should be explainable. The reviewer should see why the case was flagged, which rule or pattern was involved, what evidence was used, when the agent acted, and which person approved the next step. This audit trail is useful for internal QA, manager review, customer support, and compliance evidence. It also helps teams improve the workflow because rejected or rerouted cases reveal weak rules, poor document quality, or missing data.

For a first release, avoid broad autonomy. Let the agent recommend routing and prepare tasks, but require approval for high-risk queues, customer-facing communication, adverse-action-sensitive wording, or any decision that affects eligibility. If the team later automates low-risk routing, keep sampling, monitoring, and rollback in place.

Architecture For Loan Processing Agents

A production loan-processing agent is a workflow automation system, not just a model endpoint. It needs identity management, source connectors, document processing, retrieval, rules, prompts, tool permissions, review queues, evaluation data, and monitoring. The architecture should be narrow enough to prove value and strict enough to satisfy internal risk owners.

- Trigger: new loan application, document upload, case status change, underwriting request, compliance review, or operations ticket.

- Context: borrower application, document files, product requirements, policy documents, case notes, CRM records, and approved knowledge sources.

- Processing layer: OCR, document classification, field extraction, RAG retrieval, rules, confidence thresholds, and exception scoring.

- Action layer: draft summaries, missing-document tasks, policy answer drafts, exception recommendations, and internal notes.

- Review layer: underwriter, compliance, fraud, operations, or manager approval depending on risk and workflow stage.

- Controls: permissions, audit logs, prompt and policy versioning, evaluation sets, monitoring, alerts, and rollback.

If the team is still deciding whether a workflow is ready for agent behavior, start with the AI Agent Readiness Assessment. It forces the right questions around workflow boundaries, data quality, integrations, governance, and human review.

Human Review And Governance Model

Loan-processing agents need governance by design because their outputs touch borrower data, credit workflows, compliance evidence, and customer trust. Governance should define what the agent can see, what it can summarize, what it can change, what it can recommend, and what must be approved before anything moves forward.

A useful model separates assistance from decisioning. Low-risk assistance might include intake summaries, checklist status, or internal notes. Higher-risk actions include compliance routing, borrower communication, system updates, underwriting recommendations, and anything that could affect eligibility or required disclosures. The higher the risk, the stronger the approval gate and audit evidence should be.

Governance should also include evaluation. Track extraction accuracy, missing-document detection, summary usefulness, reviewer edit distance, approval rate, false escalations, missed escalations, cycle time, and complaint or QA signals. If reviewers constantly rewrite the output, the agent is not ready for broader workflow coverage.

For regulated lending teams, the implementation partner also matters. A governed build should connect workflow design, financial-data permissions, retrieval quality, reviewer queues, audit evidence, and model monitoring from the first pilot. NextPage's AI development services for banking and financial services are structured around those BFSI constraints rather than generic chatbot delivery.

2026 Lending AI Governance Update

In 2026, lending AI governance should be treated as an operating model, not a policy appendix. The OCC, Federal Reserve, and FDIC issued updated interagency model-risk guidance on April 17, 2026 that emphasizes a risk-based approach, model development and use, validation and monitoring, governance and controls, and vendor or third-party products. The same bulletin also notes that generative AI and agentic AI are novel and rapidly evolving, and that agencies expect to keep studying AI-specific model-risk questions. For a loan-processing agent, that means every pilot should define the model or system inventory entry, owner, approved data sources, vendor dependencies, evaluation set, monitoring cadence, and shutdown or rollback path before the agent touches production queues.

NIST's AI Risk Management Framework remains a useful cross-functional language for that work because it focuses teams on trustworthy AI design, risk management, evaluation, and governance. NIST also released a 2026 concept note for trustworthy AI in critical infrastructure and states that AI RMF 1.0 is being revised. Lending teams should treat that as a signal to keep their agent controls versioned: policy sources, retrieval indexes, prompts, model versions, test sets, monitoring thresholds, and reviewer guidance should all have owners and change history.

Adverse-action explainability is especially important. CFPB guidance says creditors using AI or complex models still need specific and accurate reasons when adverse action is taken. If an AI workflow prepares underwriting summaries, flags exceptions, or influences eligibility-related review, the lending team still needs source-backed reasons for any credit action. The agent should separate extracted facts from inferred risk signals, cite the document or policy source behind each recommendation, and make reviewer edits part of the audit trail. A fluent summary is not enough if the team cannot reconstruct why a route, condition, or denial reason was proposed.

| 2026 Control Gate | What To Prove Before Expansion | Why It Matters In Loan Processing |

|---|---|---|

| Approved-use boundary | The agent is limited to intake, document checks, retrieval, summaries, routing, or draft notes; final credit judgment stays with people. | Prevents a workflow assistant from becoming an unapproved decision engine. |

| Source-backed explainability | Each recommendation links to borrower documents, policy versions, rules, prompts, model versions, and reviewer actions. | Supports adverse-action review, audit reconstruction, QA, and compliance challenge. |

| Fair-lending and drift monitoring | Outcome, exception, edit-distance, false-escalation, and reviewer-override metrics are reviewed on a defined cadence. | Shows whether the workflow remains useful and whether errors are concentrated in sensitive borrower groups or products. |

| Third-party and model-change controls | Vendor models, OCR services, credit-data providers, document AI tools, and case-management integrations have change notices and rollback paths. | Keeps borrower-data processing, model changes, and vendor dependencies visible to risk owners. |

| Kill switch and rollback | Operations can disable the agent, route cases manually, preserve logs, and restore the prior workflow if quality or compliance signals degrade. | Turns governance from a policy statement into an operational control. |

Third-party and vendor controls also need more discipline as loan operations teams add packaged AI tools, document AI services, credit-data providers, and case-management integrations. Before expansion, confirm where borrower data is processed, which model or prompt version produced each output, how bias and drift are monitored, who can override or disable the workflow, and how the institution will respond if a vendor model changes. These controls make the agent practical for production because human reviewers can trust the evidence, challenge the output, and stop the workflow when quality or compliance signals degrade.

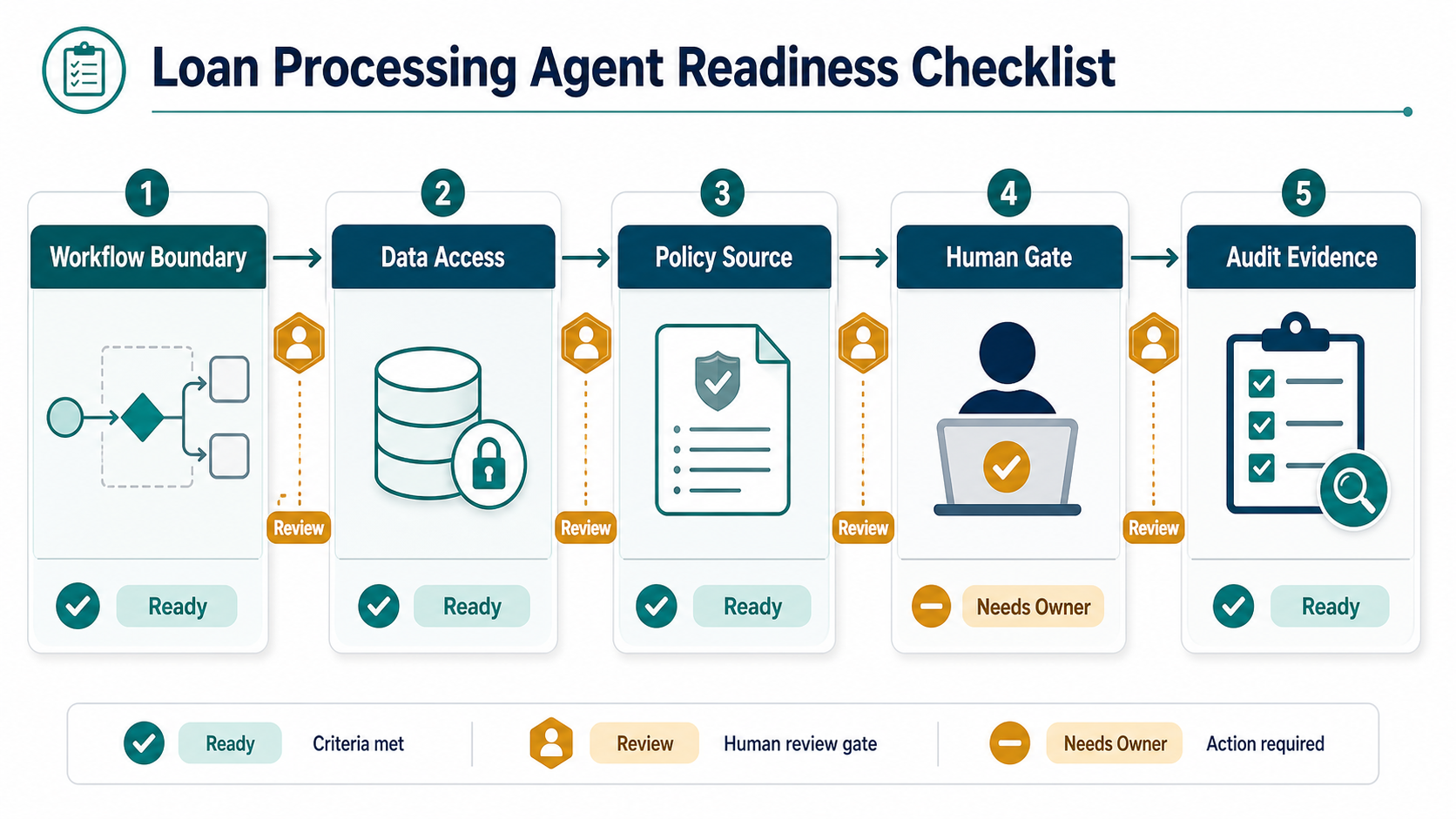

Loan Processing Agent Readiness Checklist

Before funding a pilot, confirm that the lending workflow is ready for supervised agent behavior. The workflow should have a clear owner, defined start and stop points, known document types, approved policy sources, and a review queue that can absorb exceptions. Without those basics, the agent will create more review work than it removes.

| Readiness gate | What to confirm | Why it matters |

|---|---|---|

| Workflow boundary | One loan product, queue, or document workflow has a clear scope | Prevents the pilot from becoming an open-ended automation program |

| Data access | Borrower data, documents, case notes, and system permissions are mapped | Limits sensitive access and avoids incomplete context |

| Policy source | Approved product rules, underwriting guidance, and policy versions are available | Reduces hallucinated or stale guidance |

| Human gate | Reviewers know what they approve, reject, edit, or escalate | Keeps lending judgment and compliance accountability with people |

| Audit evidence | Each recommendation records source documents, policy references, reviewer action, and timestamps | Supports QA, compliance review, and rollback |

If the team needs a quick readiness baseline, the AI Agent Readiness Assessment can score workflow clarity, data quality, integrations, governance, and human review before a full implementation plan. For larger programs, the enterprise AI readiness checklist gives risk owners a broader governance view.

Implementation Roadmap

The safest rollout starts small. Pick one workflow, prove measurable value, and expand only after the system earns trust with real review data.

| Phase | Goal | Output |

|---|---|---|

| 1. Workflow selection | Choose one high-volume, reviewable loan-processing task | Use-case brief, owner, risk notes, baseline metrics |

| 2. Data and policy mapping | Identify document types, systems, policies, roles, and access boundaries | Data map, permission model, retrieval scope |

| 3. Assistant pilot | Generate summaries, checklist status, and policy answer drafts without system writes | Reviewer feedback, accuracy measurements, issue log |

| 4. Supervised tool use | Prepare tasks, route exceptions, and draft notes for approval | Audit trail, approval workflow, rollback plan |

| 5. Scale decision | Expand to additional loan products or teams if quality and controls are proven | ROI report, governance sign-off, next release plan |

Budget and timeline depend on more than the model. Integration depth, document quality, compliance controls, exception volume, and review workflow complexity all matter. The AI agent development cost guide explains why supervised workflows, connected tool actions, and regulated data usually require more discovery, testing, and monitoring than a simple chatbot.

Metrics For Loan Processing AI

Measure operational outcomes first. Useful metrics include intake completion time, missing-document detection rate, number of files returned from underwriting for incomplete evidence, time to first review, exception routing accuracy, reviewer edit distance, queue aging, escalation rate, and audit completeness. These metrics help teams judge whether the agent improves processing quality, not just whether it produces fluent summaries.

ROI should be tied to baseline volume and review ownership. A small workflow with thousands of monthly applications may outperform an ambitious agent that touches many systems but has low usage. Measure time saved, rework avoided, quality improvements, and reviewer adoption before connecting the workflow to broader business outcomes.

Do not over-attribute approval rates, default rates, or revenue changes to an agent without a strong testing design. Loan outcomes depend on product mix, borrower quality, credit policy, rates, market conditions, staffing, and many external factors. The agent's first job is to make file preparation, evidence review, and routing more consistent.

Build, Buy, Or Customize?

Some lending teams can start with packaged loan origination, document automation, or workflow tools. Custom AI-agent development makes more sense when the process spans several systems, uses institution-specific policy, requires custom review queues, or needs a proprietary borrower or operations experience. It also makes sense when the team wants AI assistance inside an existing platform rather than a standalone tool. If the product needs bounded tool use, audit logs, human approval, and workflow orchestration, compare packaged tools with agentic AI development services before committing to architecture.

Use a build-versus-buy discussion around workflow fit, data sensitivity, integrations, policy complexity, audit requirements, and long-term ownership. If the goal is a one-off document summary, a packaged tool may be enough. If the goal is a governed workflow across intake, document AI, RAG, case management, underwriting support, and compliance review, a custom build or deep integration may be more realistic.

The fintech app development cost guide is a useful companion for budget planning because compliance, security, integrations, and reporting can be major cost drivers in financial products. Loan-processing AI agents inherit many of those same drivers. Teams comparing a custom build against packaged tooling can also use the Custom Software Cost Estimator to pressure-test integration, role, reporting, and support scope before committing.

When NextPage Can Help

NextPage helps lending, fintech, and operations teams design practical AI-agent workflows for loan processing. We start by mapping the workflow, identifying the safest first use case, reviewing data and document readiness, designing retrieval and review controls, and estimating the integration path. Then we build the assistant or supervised agent around your actual loan operations rather than forcing a generic bot into a regulated workflow.

If your team is evaluating AI agents for loan processing, start with a readiness review: one loan product, one workflow, clear review ownership, and measurable baseline metrics. From there, NextPage can scope the data model, document pipeline, RAG layer, approval gates, case-management integration, audit trail, and rollout plan needed for a responsible pilot.