Quick Answer: Where AI Fits In Insurance

AI in insurance works best when it is attached to a specific operating decision: triaging a claim, extracting document data, flagging suspicious patterns, summarizing underwriting evidence, routing service requests, or helping an agent answer a policy question. The useful question is not whether an insurer should use AI. It is which workflow has enough volume, data quality, review capacity, integration access, and business value to justify automation.

For most insurers, brokers, claims teams, and insurtech founders, the safest starting point is assisted decision-making. AI can collect evidence, classify inputs, recommend next actions, draft explanations, and prepare reviewer queues while a licensed or accountable team member approves customer-impacting decisions. That keeps speed gains from turning into compliance or trust problems.

If the workflow, data, integrations, and governance are still unclear, start with the AI Agent Readiness Assessment. If the business case needs a first-pass estimate, use the AI Automation ROI Calculator before scoping a build.

Practical AI Use Cases In Insurance

The strongest insurance AI use cases usually sit in document-heavy, rules-heavy, or exception-heavy work. Claims teams handle forms, photos, estimates, adjuster notes, repair invoices, medical records, emails, and policy language. Underwriting teams review applications, prior losses, property details, financial records, and third-party data. Service teams answer repetitive questions while still needing policy-specific context.

| Use case | AI role | Best first metric | Human review point |

|---|---|---|---|

| Claims intake | Extract fields, classify claim type, detect missing documents | Cycle time from submission to first review | Coverage, liability, payment, denial, or escalation decision |

| Underwriting support | Summarize evidence, score data completeness, compare against rules | Submission review time and quote readiness | Risk acceptance, exclusions, pricing, and referral decisions |

| Fraud triage | Detect unusual patterns, duplicate signals, network anomalies, inconsistent narratives | Investigator queue precision | Any adverse customer action or special investigation referral |

| Customer service | Answer common questions, retrieve policy context, draft responses | Resolution time and handoff rate | Complaints, coverage disputes, cancellations, and regulated notices |

| Agent enablement | Prepare account briefs, recommend next-best actions, explain product differences | Agent productivity and conversion quality | Personalized advice, binding, and complex suitability questions |

These use cases can share a common platform foundation: identity and permissions, document ingestion, retrieval, workflow orchestration, audit logs, model evaluation, and escalation routing. Building the platform once and applying it to a narrow workflow first is usually more durable than building several disconnected demos. NextPage usually treats this work as AI development services tied to operational systems, not as a prompt-only experiment.

Workflow Selection Scorecard

Before choosing a model, score candidate workflows. A claims-intake assistant may look simpler than underwriting support, but the right answer depends on volume, data access, measurable delay, customer impact, and approval complexity. A workflow is a strong first candidate when the input is common, the output can be reviewed, the improvement can be measured, and failures can be routed safely.

| Score area | Good first AI workflow | Risky first AI workflow |

|---|---|---|

| Volume | Repeated weekly work with enough examples | Rare edge cases with little historical evidence |

| Data readiness | Accessible documents, labels, statuses, and outcomes | Fragmented files with unclear ownership or inconsistent identifiers |

| Decision risk | Draft, route, summarize, or recommend with review | Automatically deny, price, or bind without mature controls |

| Integration path | Clear connection to claims, policy, CRM, or document systems | Manual copy-paste between systems with no audit trail |

| Measurement | Cycle time, review hours, precision, override rate, or service quality | Vague transformation goal with no operating metric |

This scorecard is also where AI agent development becomes relevant. Agentic workflows should be saved for cases where tool access, permissions, human approvals, and evaluation logs are ready enough for the system to act safely.

Claims Automation Without Losing Control

Claims automation is often the most visible insurance AI opportunity because customers feel every delay. AI can classify a claim, read submitted documents, extract dates and amounts, compare the file against policy rules, summarize adjuster notes, and identify missing evidence before a person opens the case.

The control design matters. A low-risk workflow may auto-route a claim or request another document. A high-risk workflow should stop at recommendation and explanation. If the output affects payment, denial, reserve changes, fraud referral, or customer rights, the workflow needs clear human approval, a versioned reason, and an audit trail.

Claims AI should also be built for exception handling. Real files contain handwritten notes, blurry images, duplicate forms, mismatched names, and policy edge cases. A production system needs confidence thresholds, fallbacks, and a queue for cases the model should not decide. The same release discipline behind a pre-launch QA checklist for custom software applies here because mistakes can affect customers, regulators, and downstream operations.

Underwriting And Pricing Support

Underwriting AI is strongest when it reduces preparation time and improves consistency. It can check whether a submission is complete, summarize risk evidence, compare applicant data against appetite rules, identify contradictory information, and prepare a referral note for senior review.

That does not mean the model should independently bind or price complex risk. In regulated and high-value contexts, AI should make the review package better: clearer evidence, faster document comparison, more consistent appetite checks, and fewer missed red flags. The underwriter still owns judgment, exceptions, and accountability.

Teams should separate decision support from decision automation. Decision support is usually easier to launch, easier to govern, and easier for underwriters to trust. Full automation can follow only after the data, monitoring, and override patterns are proven. For model-heavy scoring, classification, and prediction work, machine learning development is the more precise planning path.

Fraud Detection And Investigation Triage

Fraud detection is a natural fit for machine learning because the patterns are subtle and constantly changing. The NAIC cites Coalition Against Insurance Fraud estimates that insurance fraud costs businesses and consumers hundreds of billions of dollars each year in the United States. That scale makes even modest improvements in triage quality meaningful.

A practical fraud system should not treat an AI score as a verdict. It should rank review queues, show the signals behind the ranking, compare a case with similar historical patterns, and route suspicious files to trained investigators. The objective is better prioritization, not opaque denial.

For generative AI, fraud teams also need to watch the input side. Synthetic documents, manipulated photos, and AI-written narratives can make old manual checks weaker. That pushes insurers toward stronger provenance checks, document validation, image forensics, reviewer tooling, and incident review. Adjacent financial-services patterns appear in NextPage's machine learning guide for fraud detection and credit risk.

Customer Service And Agent Assistance

AI assistants can help service teams answer policy questions, summarize past interactions, draft emails, explain claim status, and hand off complex requests. The best assistants are grounded in approved documents and live policy context rather than generic model memory.

For insurance, customer service AI should be conservative. It should quote source material, explain uncertainty, and escalate when the question involves coverage interpretation, complaints, cancellation, claims disputes, or legal language. A good assistant reduces handle time without pretending that every policy question is simple.

Agent enablement is another strong fit. AI can prepare renewal notes, compare product options, identify missing client data, and suggest next-best actions. These workflows improve productivity while keeping licensed advice and final communication under human control. If the use case is service-heavy, the implementation details in AI customer service agent integration are a useful supporting pattern.

Data Readiness Before AI Development

Insurance AI fails more often from weak data plumbing than weak model choice. Before development, map the systems involved: policy administration, claims management, CRM, document storage, email, call transcripts, payment data, third-party enrichment, and reporting. Then check whether the target workflow has enough clean examples to test the model.

- Data access: Can the AI system read the right policy, claim, customer, and document records with scoped permissions?

- Data quality: Are labels, statuses, dates, document types, and identifiers consistent enough for automation?

- Data lineage: Can reviewers see where a recommendation came from?

- Evaluation data: Do you have examples of correct outcomes, edge cases, and unacceptable outputs?

- Retention and privacy: Are sensitive records handled according to internal and regulatory requirements?

This is where a custom implementation often beats a generic tool. The model layer may be small, but the integrations, permissions, evaluation harness, and audit trail determine whether the system can run inside a real insurance operation. For teams that need this foundation, NextPage's custom software development work is the closest fit.

Risk, Compliance, And Human Review Controls

Insurance AI touches sensitive data and high-impact decisions. That makes governance a product requirement, not an afterthought. NAIC's 2023 AI model bulletin and 2025 AI systems evaluation resources emphasize governance, risk management, validation, testing, and accountability for insurer AI use. Those expectations should shape the product backlog before a production release.

At minimum, production insurance AI should include role-based access, prompt and policy versioning, source citations for generated answers, approval queues, audit logs, test suites, fallback rules, incident reporting, and periodic model review. For generative AI, add retrieval boundaries so the assistant answers from approved material rather than improvising.

Human review should be designed around risk. Auto-routing a document is different from denying a claim. Summarizing an underwriting file is different from changing premium. Each action needs a clear autonomy level, from draft only to recommend to execute after approval to execute automatically for low-risk cases. The same governance logic is expanded in the enterprise AI readiness checklist and enterprise AI agent governance guide.

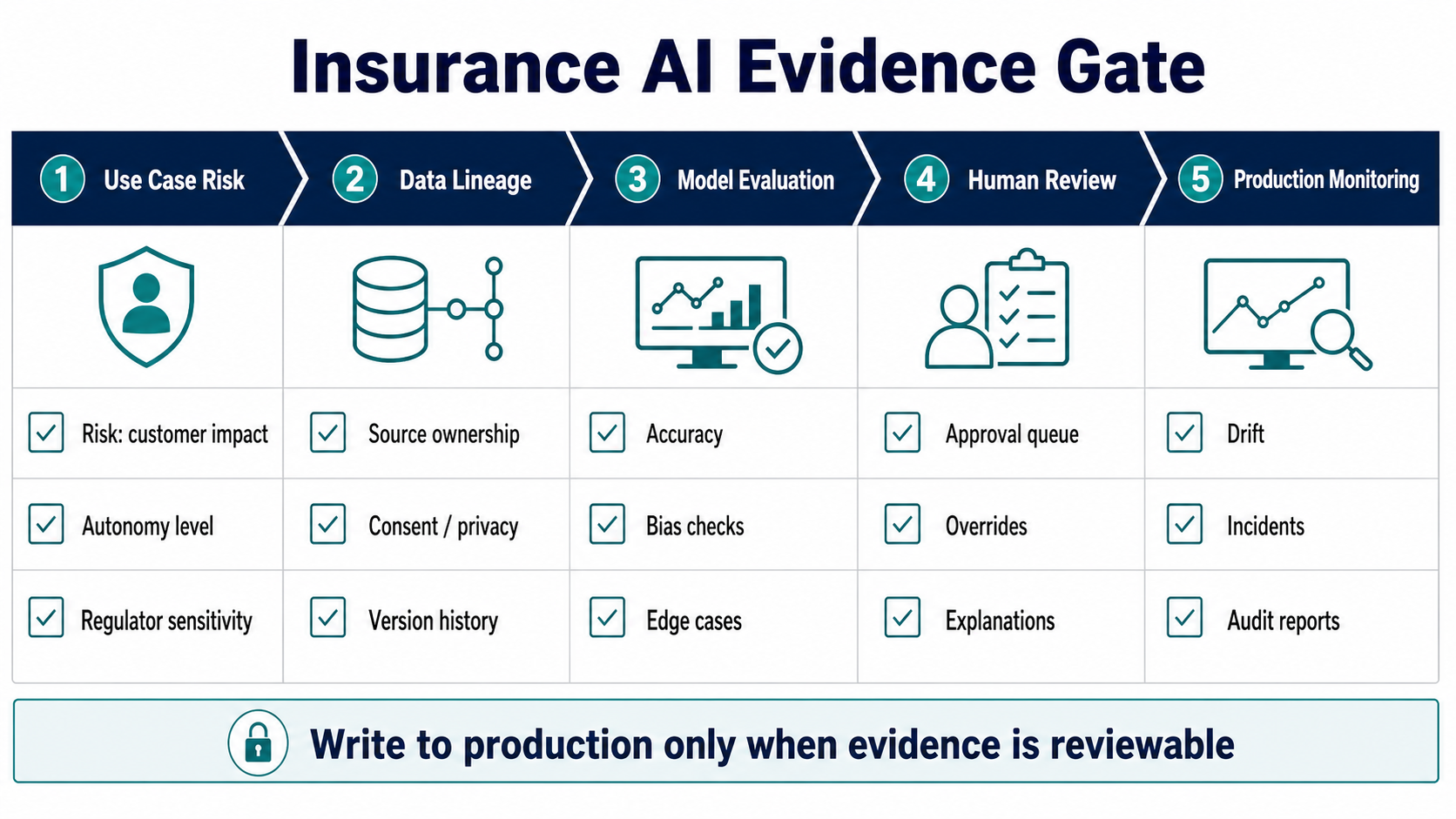

Insurance AI Evidence Gate Before Production

A production gate keeps an AI pilot from becoming an unmanaged operating dependency. Before launch, require evidence for the use case risk, data lineage, evaluation results, human review path, and production monitoring. The evidence does not need to be bureaucratic, but it must be reviewable.

- Use case risk: name customer impact, autonomy level, regulatory sensitivity, and escalation requirements.

- Data lineage: document source systems, ownership, consent or privacy constraints, and version history.

- Model evaluation: test accuracy, bias risks, edge cases, drift triggers, and unacceptable outputs.

- Human review: define approval queues, override capture, explanations, and accountable owners.

- Production monitoring: track drift, incidents, audit reports, cycle-time impact, reviewer acceptance, and customer outcomes.

ROI And Operating Metrics For Insurance AI

Insurance AI ROI should be measured with operational metrics, not model novelty. Claims leaders may care about first-touch time, document completeness, adjuster review hours, supplement cycle time, leakage reduction, and customer updates. Underwriting leaders may care about submission completeness, referral quality, quote turnaround, appetite-rule consistency, and producer experience. Fraud teams may care about investigator queue precision, avoided leakage, false positives, and time to evidence.

Choose one primary metric and two or three guardrail metrics before the pilot starts. For example, a claims intake assistant might target a shorter time from submission to first review while guarding against higher complaint rate, higher adjuster override rate, or missed high-risk files. An underwriting assistant might target faster review packages while guarding against poor explanation quality or excessive referral noise.

| Workflow | Primary ROI metric | Guardrail metric | What to review weekly |

|---|---|---|---|

| Claims intake | Cycle time to first review | Missing-document rework | Low-confidence cases and override reasons |

| Underwriting support | Submission review time | Referral quality and appetite-rule misses | Evidence summaries underwriters rejected |

| Fraud triage | Investigator queue precision | False positives and adverse-action risk | Signals that produced useful evidence |

| Service assistant | Resolution time or handoff rate | Complaint escalation and answer grounding | Questions where citations were weak |

Those operating reviews create the feedback loop that turns a pilot into a production system. Without them, teams can ship an impressive demo that no one trusts when edge cases arrive.

Ownership After Launch

The most common insurance AI failure is assuming the project ends when the model goes live. Production ownership needs named people for source-data changes, policy changes, prompt or model updates, review queues, incident response, evaluation examples, and executive reporting. If those owners are missing, the system will drift quietly while the business assumes it is still working.

Assign owners across product, operations, compliance, data, engineering, and support. Product owns the business outcome. Operations owns reviewer workflows and exception handling. Compliance or legal owns regulated notices and audit expectations. Data owners maintain source quality and lineage. Engineering owns integration reliability, monitoring, and rollback. Support captures customer-facing confusion that might not appear in model metrics.

This operating model is why insurance AI belongs inside a broader software delivery plan. The model may classify, summarize, retrieve, or predict, but the surrounding system must route work, preserve context, collect feedback, protect sensitive records, and help humans make defensible decisions.

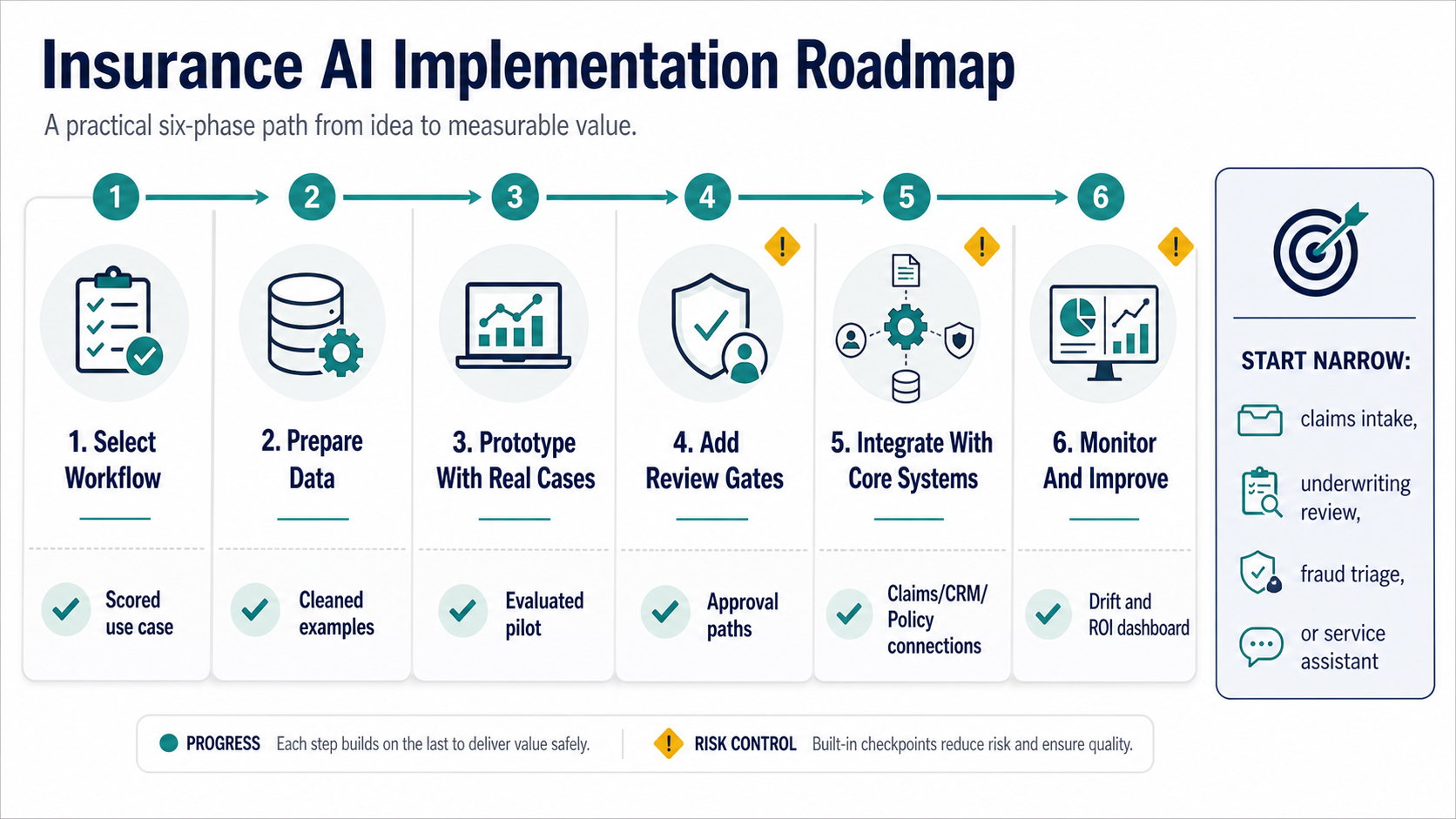

Implementation Roadmap

A sensible insurance AI roadmap starts narrow. Choose one workflow where success can be measured, such as claim intake completeness, underwriting submission review time, fraud triage precision, or service response drafting. Define what the AI can decide, what it can only recommend, and what must always go to a human.

- Select the workflow. Score candidates by volume, manual effort, error cost, data availability, and compliance risk.

- Prepare the data. Clean labels, normalize documents, map systems, and define permission boundaries.

- Prototype with real cases. Test rules, ML, retrieval, and generative AI against historical examples.

- Add review gates. Route low-confidence, high-value, disputed, or regulated decisions to people.

- Integrate with operations. Connect the AI output to claims, underwriting, CRM, policy, and document systems.

- Monitor and improve. Track accuracy, cycle time, override rate, customer impact, drift, and ROI.

When the workflow includes repeated actions across systems, the Workflow Automation Opportunity Finder can help separate automation candidates from process problems that should be cleaned up first.

Build, Buy, Or Integrate?

Buy when the workflow is standard, the vendor already integrates with your core systems, and the controls meet your compliance requirements. Build when the workflow is a competitive differentiator, the data model is unique, or the system needs deep integration across policy, claim, CRM, and document stores. Integrate when a vendor handles a narrow model task but your team still needs a custom operating layer around it.

A common hybrid pattern is to use proven model or document-intelligence services inside a custom workflow. That lets the insurer keep ownership of permissions, review queues, business rules, analytics, and customer experience while still benefiting from mature AI components. If the decision is still open, NextPage's Build Vs Buy Decision Tool gives stakeholders a structured way to compare vendor fit, operating ownership, integration depth, and differentiation.

Portfolio patterns such as the HeatPilot case study show why recommendation and scoring surfaces need evidence, controls, and operating context around the AI output. The same principle applies to insurance: the model is useful only when the workflow can trust, review, and act on it.

How NextPage Can Help

NextPage approaches AI in insurance as product engineering: workflow discovery, data and integration mapping, risk controls, prototype design, review interfaces, production deployment, and ongoing improvement. The model is only one part of the system.

A practical first engagement can focus on one insurance workflow: claim intake triage, document extraction, underwriting submission review, service assistant grounding, fraud investigation queueing, or agent enablement. From there, the roadmap can define the integrations, evaluation examples, governance controls, and rollout plan needed to move beyond a demo.

If you are planning an AI insurance workflow, start with the work that creates measurable delay or review cost today. Keep the first release narrow, make the decision boundary explicit, and build the feedback loop before expanding autonomy.