Quick Answer: FinTech App Development Cost

FinTech app development cost usually starts with product risk, not screen count. A lightweight finance MVP with onboarding, account views, basic payments, notifications, admin controls, and analytics can often be planned around $45,000-$90,000. A regulated fintech MVP with KYC, transaction workflows, wallet or banking integrations, role-based admin operations, audit trails, and security testing often moves into the $90,000-$220,000 range. A scale platform with ledger architecture, reconciliation, fraud monitoring, open banking APIs, compliance evidence, data warehousing, and high-availability operations can move past $220,000 and into the $450,000+ range.

Those are planning bands, not quotes. The final estimate changes when you decide whether the product holds funds, initiates payments, stores card data, integrates with banks, uses third-party KYC, supports business accounts, handles lending decisions, or needs a regulated partner approval process. If you need a directional estimate before discovery, start with the Custom Software Cost Estimator, then validate the assumptions with product, engineering, security, and compliance stakeholders.

The reference article from SparxIT gives a broad market-style range, including MVPs from about $15,000-$100,000 and outsourcing builds up to $300,000. NextPage treats those figures as a sanity check, then scopes the work around product category, regulated data flows, integration depth, audit evidence, and the operating model needed after launch.

What You Are Actually Building

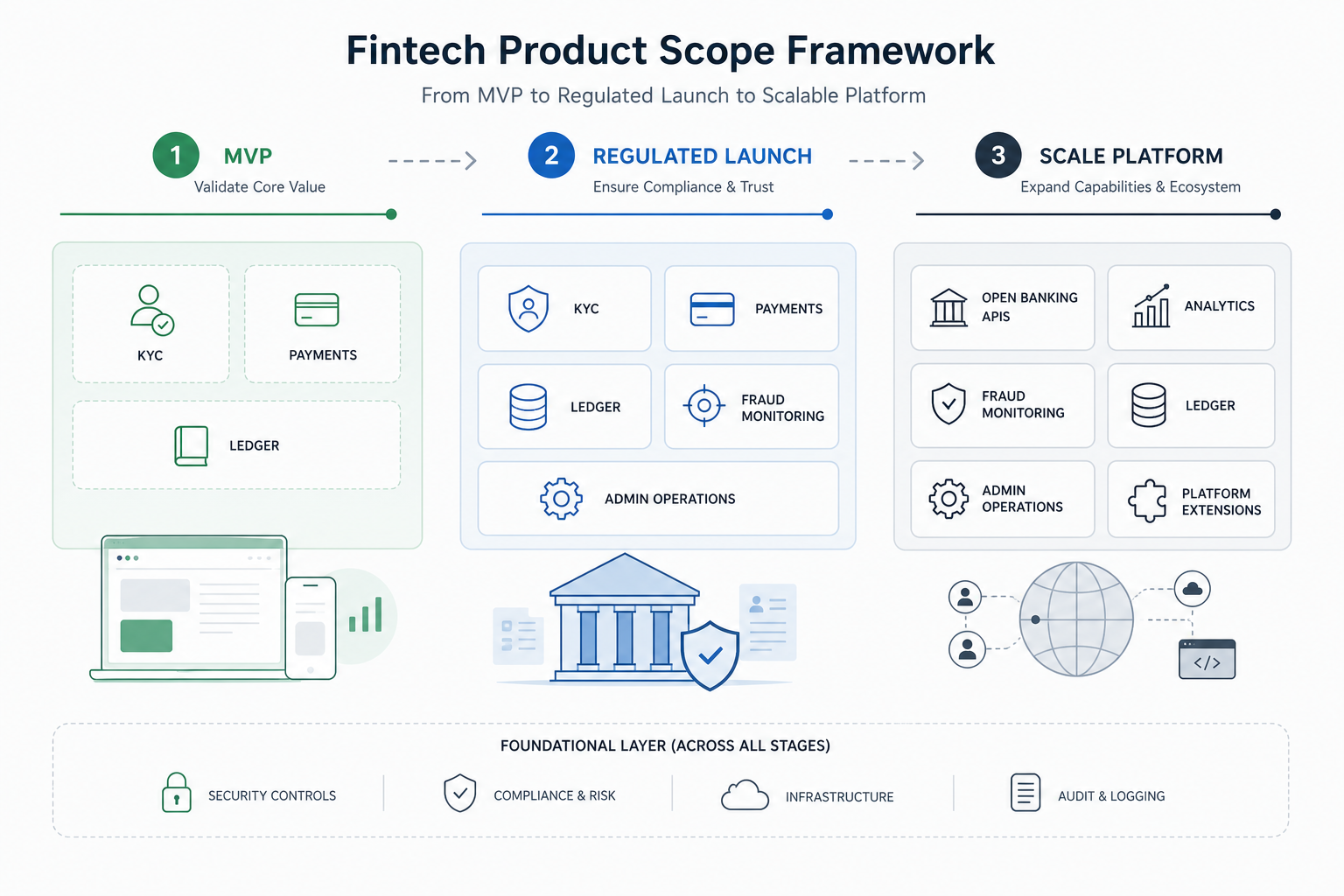

A fintech app is rarely just a mobile interface. It is usually a secure product system made of customer onboarding, identity checks, account or wallet views, payment events, transaction history, risk controls, admin operations, customer support, reporting, and partner integrations. A budgeting app has a different cost profile from a lending platform, neobank, digital wallet, insurance workflow, investment app, or embedded finance product.

This is why a fintech estimate should begin with the product's role in the financial flow. Does it only display data from another provider? Does it initiate payments? Does it store sensitive payment information? Does it make risk or credit decisions? Does it need bank, card, bureau, payroll, tax, or insurance integrations? Each answer changes architecture, quality assurance, legal review, and launch readiness.

For mobile-first fintech products, NextPage usually starts with a mobile app development plan and adds backend, security, and compliance work around the app. If the core value lives in complex workflows or back-office operations, the estimate may resemble a Custom Software Development Cost engagement more than a simple app build.

Cost Bands By FinTech Product Type

Fintech cost bands are easiest to understand by product archetype. The same feature name can mean very different engineering work depending on whether the product is advisory, transactional, regulated, or operationally complex.

| Product Type | Typical Scope | Planning Range | What Raises Cost |

|---|---|---|---|

| Finance Utility MVP | Signup, profile, dashboard, linked accounts or manual inputs, alerts, basic admin, analytics | $45,000-$90,000 | Native apps, data-provider APIs, advanced personalization, subscriptions, richer dashboards |

| Transactional FinTech MVP | KYC, wallet or payment workflows, transaction history, support console, audit trail, partner APIs, reporting | $90,000-$220,000 | Money movement, multi-party roles, PCI scope, fraud checks, reconciliation, complex refunds, partner certification |

| Regulated Scale Platform | Ledger, settlement workflows, compliance evidence, risk monitoring, multi-region operations, data warehouse, high availability | $220,000-$450,000+ | Open banking, lending or investment decisions, SOC 2 readiness, bank-grade controls, SLA operations, advanced AI risk models |

A lending app, for example, may spend heavily on underwriting workflow, document handling, disclosures, risk rules, and servicing operations. A wallet may spend more on payment processor integration, ledger consistency, chargebacks, refunds, and account controls. An investment product may need market data, suitability checks, portfolio views, compliance logs, and more exact customer communication flows.

MVP Scope That Controls Risk

A strong fintech MVP proves the customer workflow while keeping regulated complexity controlled. The first release should clarify user identity, account setup, core transaction or insight flow, customer communication, admin handling, support escalation, reporting, and the evidence needed for internal review. It should avoid pretending that every future product line must ship in the first version.

A practical MVP may use third-party KYC, hosted payment fields, banking-as-a-service providers, card network partners, and standard cloud security controls to reduce early scope. The trade-off is vendor dependency. You still need clean data models, reliable event logs, user consent records, monitoring, and an architecture that can evolve when volume, geography, or regulatory duties increase.

When the first release includes web dashboards or operations portals, compare that scope against Web App Development Cost. Fintech back-office work often grows quietly because support, reviews, disputes, reconciliations, exports, and audit trails must be usable by internal teams, not only by developers.

Compliance And Security Cost Drivers

Compliance cost depends on what the product does and where it operates. For U.S.-facing products, the CFPB's personal financial data rights rule is part of the open banking planning context because it pushes secure consumer-authorized data access and third-party obligations. The FTC Safeguards Rule is relevant for covered financial institutions because it requires an information security program for customer information. PCI DSS v4.0.1 matters when the product stores, processes, or transmits cardholder data, or when payment architecture can reduce that scope.

KYC, AML, sanctions screening, suspicious activity handling, privacy notices, consent capture, vendor due diligence, incident response, retention policies, and audit logs can all become product requirements. These are not only legal documents. They shape onboarding screens, admin workflows, data retention, access controls, logging, alerts, QA cases, and release gates.

Security layers also affect budget. Fintech apps commonly need strong authentication, device and session controls, encryption, tokenization, least-privilege access, secret management, vulnerability scanning, dependency review, secure SDLC practices, monitoring, backup and recovery plans, and penetration testing. A low-risk prototype can keep this lean. A product handling money movement or sensitive financial data needs security evidence from the start.

Integrations, Ledger, And Reconciliation

Integrations often drive more fintech cost than visible features. Payment processors, KYC vendors, banking APIs, card issuing platforms, credit bureaus, payroll providers, accounting systems, notification tools, support systems, analytics stacks, and data warehouses all have different API behavior, sandbox quality, error states, rate limits, and approval steps.

The biggest architecture decision is whether the app needs an internal ledger. A read-only finance app may only store external account snapshots and user preferences. A wallet, lending, rewards, or payment product usually needs a reliable ledger model, idempotent events, reconciliation jobs, refund and reversal logic, settlement reporting, and admin tools for investigating mismatches. That work is not optional once the product becomes transactional.

If you are comparing internal hiring, freelancers, and an outsourced team for a fintech build, the Software Development Outsourcing To India guide and the Dedicated India Team Cost Calculator can help model team cost separately from product scope.

AI, Automation, And Fraud Detection Scope

AI can improve fintech products, but it should be scoped carefully. Useful early applications include support triage, document classification, transaction categorization, anomaly review queues, collections prioritization, and financial insight generation. Higher-risk uses such as credit decisions, fraud blocking, investment advice, or automated account restrictions require stronger explainability, model monitoring, human review, data governance, and appeal workflows.

An AI feature can start as a decision-support tool rather than a fully automated decision maker. That reduces launch risk and gives the team data for measuring false positives, customer impact, reviewer productivity, and operational savings. For repeated operational tasks, the AI Automation ROI Calculator is useful for deciding whether automation has enough volume to justify custom build cost.

Team, Timeline, And Delivery Plan

A finance utility MVP often takes 12-18 weeks with a lean product team: product manager, UX/UI designer, mobile or full-stack engineers, backend engineer, QA, and DevOps/security support. A transactional fintech MVP usually needs 18-32 weeks because integrations, audit trails, error states, and security testing must be designed and tested together. A scale platform is usually delivered in release waves over 6-12 months or more.

| Phase | Typical Work | Output |

|---|---|---|

| Discovery And Risk Mapping | Product archetype, regulated flows, user roles, data map, vendor shortlist, launch geography, MVP cuts | Scope, architecture plan, assumptions, estimate, and compliance questions |

| Prototype And Validation | Onboarding, dashboard, transaction flow, admin workflow, design system, API feasibility checks | Clickable prototype and validated integration plan |

| MVP Build | Apps, backend APIs, KYC/payment integration, admin console, audit logs, notifications, reporting | Testable release candidate with operational workflows |

| Security And Launch Readiness | Threat modeling, access control review, test evidence, monitoring, support scripts, partner checks | Launch checklist and risk register |

| Scale Releases | Ledger depth, reconciliation, AI review queues, data warehouse, open banking, advanced analytics | Roadmap tied to volume, compliance, and economics |

Feature Checklist By Module

A realistic estimate groups features by module so stakeholders can see which teams and risks are driving cost.

| Module | MVP Features | Growth Features |

|---|---|---|

| Customer App | Signup, MFA, profile, dashboard, account views, transactions, alerts, help | Personalization, budgeting, insights, subscriptions, multi-account controls, multilingual UX |

| Identity And Risk | KYC vendor flow, consent capture, risk flags, manual review queue | AML monitoring, sanctions checks, fraud scoring, case management, reviewer analytics |

| Payments And Ledger | Payment provider integration, transaction records, basic refunds, admin search | Internal ledger, reconciliation, settlement reports, chargebacks, multi-currency, payouts |

| Admin Operations | Users, cases, transactions, support notes, exports, audit logs | Role-based workflows, approvals, policy rules, partner reporting, incident tools |

| Data And Compliance | Event logs, privacy records, basic dashboards, backup checks | Data warehouse, model monitoring, compliance evidence, retention automation, SLA reports |

Budget Mistakes To Avoid

The most common mistake is estimating fintech like a normal consumer app. The second is treating KYC, AML, PCI, privacy, and security as late-stage paperwork instead of product requirements. The third is integrating a payment or banking provider before confirming approval steps, sandbox behavior, settlement rules, and support responsibilities. The fourth is underbuilding admin operations, where disputes, reviews, reversals, compliance evidence, and customer support actually happen.

Another mistake is building a custom ledger too late or too early. Too late creates reconciliation pain and brittle fixes. Too early can burn budget before the product model is proven. The right decision depends on whether the product moves money, owns balances, handles reversals, or must prove exact transaction state to partners and auditors.

Also budget for maintenance. Fintech products need ongoing work for security patches, dependency updates, partner API changes, compliance updates, mobile OS changes, monitoring, incident response, vendor reviews, analytics, and support tooling. A planning model should reserve 20-30% of the initial build budget per year for maintenance and continuous improvement when the product is transactional or regulated.

How NextPage Scopes FinTech Products

NextPage scopes fintech products by mapping the money, data, identity, and operational flows before estimating screens. We identify the product archetype, customer journey, regulated actions, partner dependencies, security controls, admin responsibilities, reporting needs, and post-launch support model. Then we split the roadmap into MVP, regulated launch, and scale releases so the first budget goes toward the workflows that prove value without hiding risk.

For a budgeting app, that may mean secure account linking, dashboards, notifications, and retention loops. For a wallet or payment product, it may mean KYC, payment flows, transaction state, reversals, reconciliation, and support tooling. For a lending or insurance workflow, it may mean document capture, eligibility rules, review queues, disclosures, and evidence trails.

If you are planning a fintech product, estimate the first release with the Custom Software Cost Estimator, then use a discovery sprint to validate integrations, compliance assumptions, security controls, and operating workflows behind the number.