Quick Answer: What Does A Mobile Banking App Cost?

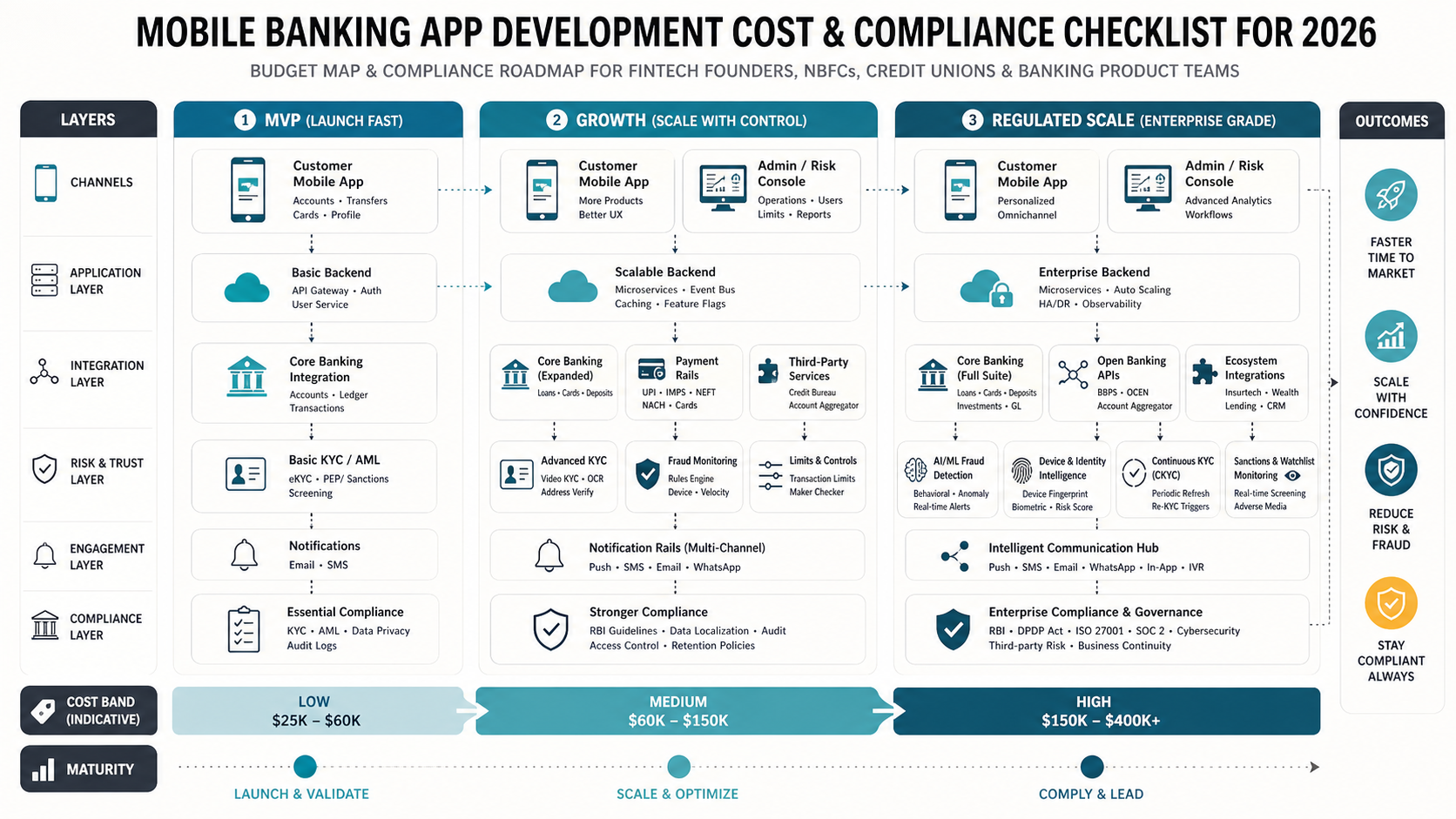

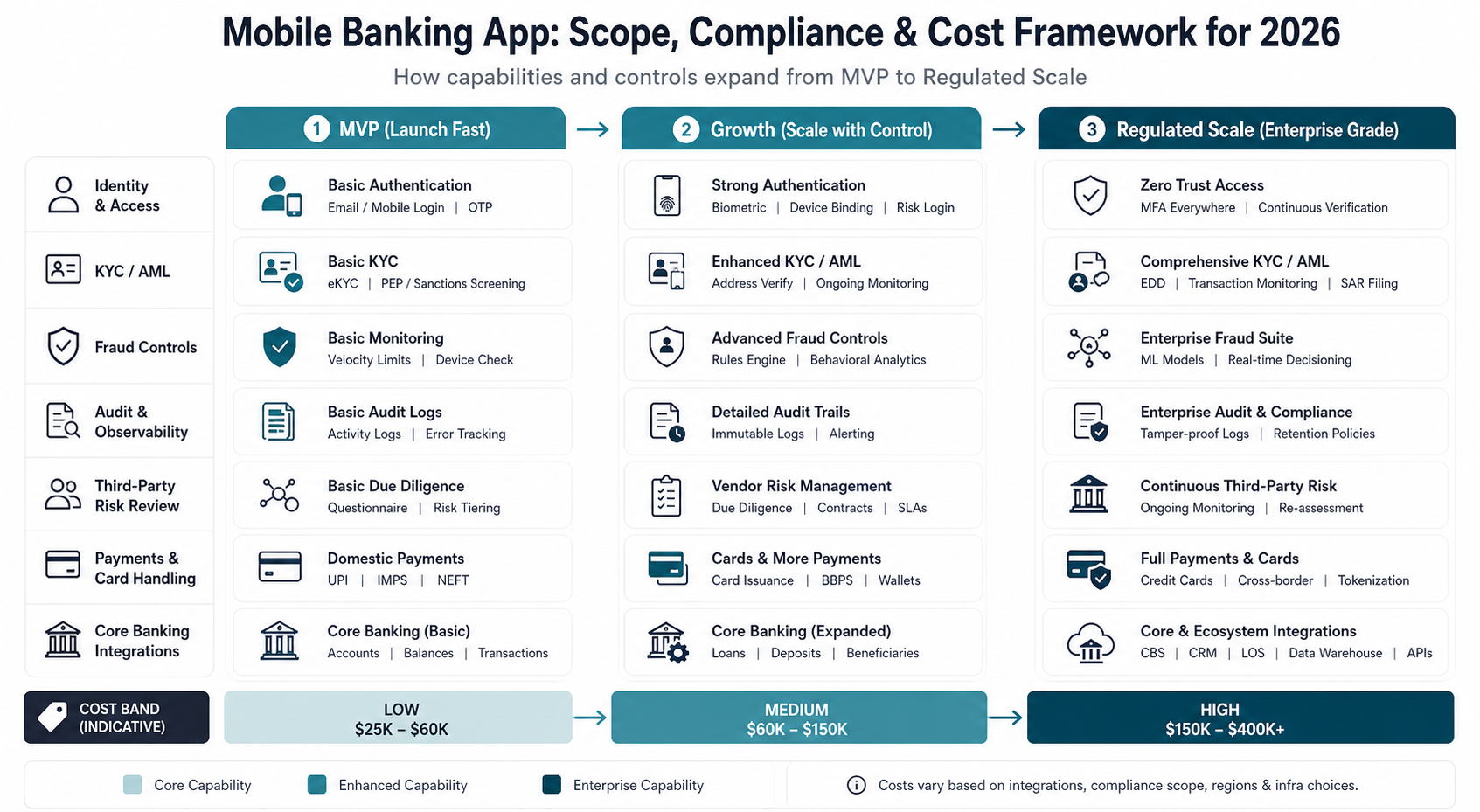

A mobile banking app usually lands in one of three planning bands. A tightly scoped MVP that covers secure sign-in, balances, transaction history, transfers, notifications, a simple admin layer, and baseline KYC workflows can start around $25,000-$60,000 when the institution already has a clear product boundary and key vendors selected. A stronger growth-stage release with richer onboarding, card controls, bill pay, fraud checks, better analytics, and more operational tooling often moves into the $60,000-$150,000 range. A regulated-scale product with broader product lines, deeper core-banking integrations, advanced auditability, open-banking or data-sharing interfaces, and enterprise governance usually starts around $150,000 and can move past $400,000.

The budget rises less because the app has more screens and more because the product touches more risk. Identity, KYC and AML, fraud monitoring, third-party reviews, card data boundaries, audit trails, customer support workflows, and core-banking integrations all change the delivery plan. That is why a banking app budget should be scoped as a product-and-controls problem, not a UI project.

If you need a directional number before full scoping, use the Custom Software Cost Estimator and then narrow the fintech-specific requirements from there. For broader benchmarks, compare the risk model with NextPage's FinTech App Development Cost guide so the banking-specific controls do not get hidden inside a generic app estimate.

What Pushes The Budget Up Fastest?

The biggest cost jumps usually come from the layers around the customer app.

- Identity and authentication: device binding, strong MFA, biometric fallback, session policy, recovery flows, and fraud-aware login rules all add real design and backend work.

- KYC, AML, and risk controls: document capture, sanctions screening, beneficial-owner handling for business onboarding, ongoing monitoring, case review, and maker-checker logic are often more expensive than the account dashboard itself.

- Core integrations: the difficulty of connecting to your core banking stack, payment rails, card processor, notification providers, analytics, and CRM usually changes the budget more than visual polish.

- Audit and observability: immutable logs, alerting, operational dashboards, reconciliation paths, and incident-review evidence become essential as the app handles more money movement and support traffic.

- Vendor governance: sponsor-bank reviews, third-party due diligence, contract controls, and recurring reassessment add delivery time even when the code changes seem small.

- Rollout complexity: one geography, one product line, and one customer segment are cheaper than a platform that has to support cards, lending, multiple entities, or multiple compliance regimes from the first release.

This is why a scope-first release matters. In many fintech cases, the right first step is a narrow, validated launch shaped through the MVP Scope Builder, not a full neobank-style roadmap from day one. For KYC and AML workflow design, also compare the operating model in AI Compliance Automation For Banks: regulated review needs evidence, routing, and human approval paths before automation expands.

MVP, Growth, And Regulated-Scale Budget Ranges

| Phase | Typical scope | Indicative budget band | What pushes it higher |

|---|---|---|---|

| MVP | Secure sign-in, balances, transaction history, transfers, alerts, basic KYC, limited admin tooling | $25k-$60k | Custom onboarding, multiple payment rails, deeper fraud controls, native apps plus web at launch |

| Growth | Stronger onboarding, richer account actions, bill pay or card controls, analytics, better operations, more integrations | $60k-$150k | Advanced KYC and AML workflows, case management, vendor orchestration, cross-team admin roles |

| Regulated scale | Multiple products, enterprise audit and compliance, richer risk controls, partner ecosystem, open APIs, multi-entity operations | $150k-$400k+ | Complex core-banking programs, cross-border flows, card-data scope, partner-bank governance, multi-region rollout |

These are planning bands, not fixed quotes. Existing vendor contracts, whether the institution already has a sponsor-bank relationship, whether a core platform exposes useful APIs, and how much operational tooling must ship with the first release can move the number significantly.

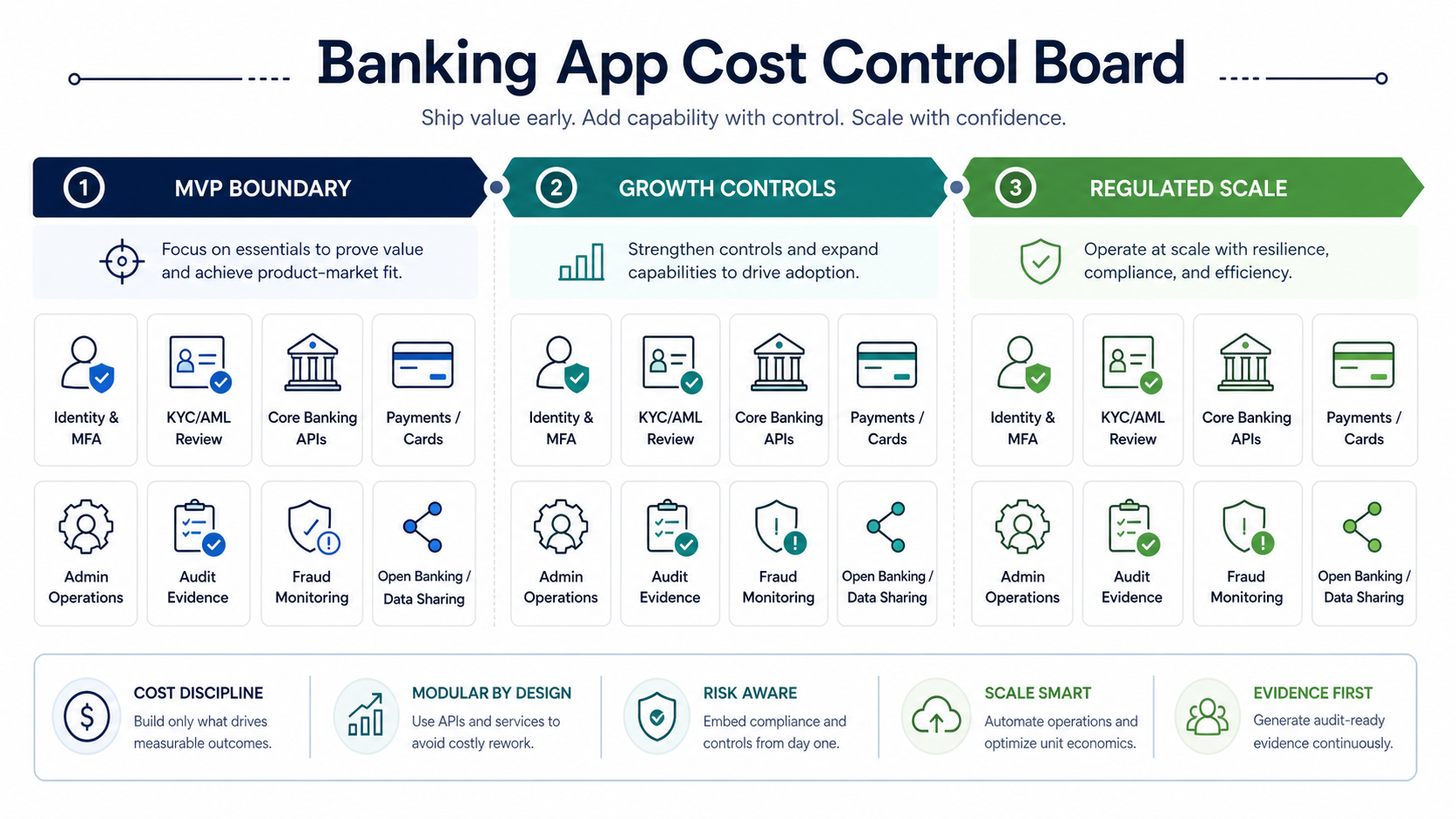

Banking App Cost Control Board

Before adding features, separate the banking-app budget into three control zones. The MVP boundary should prove safe account access, limited money movement, support visibility, and reviewable onboarding. Growth controls add richer self-service, card or payment actions, fraud signals, analytics, and operational queues. Regulated scale adds deeper audit evidence, vendor governance, high availability, data-sharing interfaces, and partner or multi-entity operating rules.

| Control Zone | Scope To Fund First | What To Defer Until Proven |

|---|---|---|

| MVP Boundary | Secure sign-in, limited account views, basic transfers, baseline KYC handoff, admin review, and support visibility. | Multiple product lines, complex personalization, and broad partner ecosystem work. |

| Growth Controls | Card controls, fraud signals, case queues, richer notifications, analytics, and stronger reconciliation paths. | Full enterprise governance, open APIs, and multi-entity operations unless they are launch-critical. |

| Regulated Scale | Audit evidence, vendor monitoring, high availability, data-sharing interfaces, and formal operating controls. | Custom automation that lacks compliance ownership, user evidence, or operational review paths. |

2026 Compliance Checklist Before You Scope

For 2026 planning, treat compliance as a workstream that shapes scope from the start.

- Authentication and identity: NIST finalized SP 800-63-4 on August 1, 2025. If your product needs higher assurance, strong MFA, device trust, phishing-resistant authenticators, and reliable recovery flows should be treated as architecture decisions, not polish items added at the end.

- Mobile-channel risk management: FFIEC's mobile financial services guidance still matters because it frames mobile banking as an enterprise-wide risk program across device security, authentication, data protection, application security, transmission security, compliance, and third-party management.

- Customer due diligence: FinCEN's CDD rule still requires covered institutions to identify and verify customers and beneficial owners of legal-entity customers, then maintain risk-based ongoing due-diligence procedures. That changes onboarding, admin review, storage, and audit requirements.

- Third-party risk: the interagency third-party risk guidance issued June 6, 2023 by OCC, the Federal Reserve, and the FDIC covers the full life cycle of third-party relationships: planning, due diligence, contract negotiation, ongoing monitoring, and termination. If your app depends on fintech vendors, this affects schedule as much as coding does.

- Data portability and open-banking interfaces: if your roadmap includes U.S. consumer-permissioned data sharing, note that the CFPB finalized the personal financial data rights rule in October 2024, but the CFPB's implementation page says the compliance dates were stayed by the court on October 29, 2025 and the Bureau is considering amendments. That means API-sharing scope can still move.

- Payments and card handling: if the app stores, processes, or transmits cardholder data, PCI SSC's current document library centers on PCI DSS v4.0.1. Many teams reduce scope by pushing payment-card handling to compliant providers instead of owning more of the card-data boundary themselves.

The right takeaway is not to panic. It is to separate what your app must control directly from what should be delegated to sponsor banks, card issuers, KYC vendors, fraud tools, or compliant processors.

Feature Stack By Product Layer

A mobile banking product usually breaks into five layers.

- Customer layer: sign-in, balances, transaction history, transfers, bill pay, beneficiary management, statements, profile controls, notifications, and support access.

- Risk and trust layer: OTP or passkey flows, device intelligence, KYC and AML checks, sanctions screening, suspicious-activity review, limits, holds, and fraud signals.

- Operations layer: admin console, maker-checker actions, case review queues, support tooling, role-based access, exception handling, and audit trails.

- Integration layer: core banking, payment rails, cards, KYC vendors, messaging providers, CRM, analytics, and data exports.

- Governance layer: policies, evidence capture, logging, observability, data-retention controls, and vendor-risk review.

Most teams should not build every layer to maximum depth in release one. A stronger first release is usually a narrow product with reliable account access, safe money movement, clear admin controls, and visible operational evidence. That is the kind of product boundary we typically shape through mobile app development and broader custom software development planning together.

Timeline For A Mobile Banking App Build

A practical delivery timeline often looks like this.

- Discovery and compliance mapping: 2-4 weeks to define product scope, institution type, control boundaries, vendor map, operational owners, and first-release success criteria.

- Architecture and MVP build: 8-14 weeks for customer flows, backend services, onboarding, notifications, admin tooling, QA, and release preparation.

- Growth release: 6-10 more weeks for richer onboarding, stronger risk controls, additional integrations, analytics, and support workflows.

- Regulated-scale expansion: 10-20 more weeks for broader product lines, enterprise audit controls, partner or sponsor workflows, data-sharing interfaces, and additional governance requirements.

The most common timeline mistake is mixing phase-one validation goals with phase-three regulatory or partner ambitions. If the first release only needs to prove customer adoption and a safe operating model, do not fund every advanced feature before the institution has validated the operating workflow. Sensitive automation should follow the same approval-gate thinking described in the Secure AI Agent Development Checklist: define the allowed action, approval path, logs, and rollback process before software acts on regulated data.

Build Web Only, Mobile Only, Or Both?

Many banking products eventually need both a mobile surface and some responsive or web-based support workflows. The question is what the first release must prove.

A mobile-first launch makes sense when the main value is customer access, account visibility, notifications, and fast everyday actions. A web-first or hybrid start can be smarter when operations, support, or onboarding review matter more than pure mobile adoption. The decision also depends on how much platform-specific work you want in version one. If that trade-off is still unclear, compare the release implications in this overview of native vs cross-platform mobile app development.

What matters most is not the framework debate by itself. It is whether the chosen stack supports your authentication model, vendor SDK constraints, release cadence, and long-term maintenance burden.

When Vendor Choice Changes Cost

Vendor selection can change the budget more than a new feature. If your institution already has trusted KYC, card, messaging, fraud, and core-banking vendors with clear APIs, the build can stay focused on product orchestration. If those relationships are still undecided, engineering has to absorb discovery risk, fallback logic, environment constraints, and contract uncertainty.

This is also where infrastructure choices matter. A safer fintech roadmap often needs environment isolation, access controls, release automation, and evidence-friendly observability before the institution is comfortable scaling the app. If that boundary is still immature, the work starts to overlap with cloud migration services and cloud-foundation planning rather than pure app delivery.

Mistakes That Inflate Banking App Budgets

- Starting like a full neobank: too many teams try to ship the end-state platform before the first product boundary is proven.

- Treating compliance like a later checklist: identity, due diligence, fraud, audit, and vendor reviews shape architecture from the start.

- Ignoring admin workflows: support teams, compliance reviewers, and operations managers often determine whether the product is workable in production.

- Owning too much card or payment scope: pushing the wrong flows inside your own boundary can increase both cost and review overhead.

- Underestimating integration quality: the budget breaks when every vendor has a different reliability model and no one planned for fallback paths.

- Choosing a stack before the risk model: authentication, vendor SDKs, and review processes should influence platform choices, not the other way around.

How NextPage Scopes Secure Fintech Products

NextPage starts with the workflow boundary, the risk boundary, and the business goal. For a mobile banking product, that usually means deciding what the first release must prove, which controls belong in-house versus with trusted partners, which integrations are mandatory at launch, and what evidence the institution needs to operate with confidence.

From there, we shape the product into the smallest release that can safely deliver customer value, then expand into richer onboarding, analytics, fraud controls, additional products, and broader governance only when the economics justify it. If you are planning a secure fintech app, start with the Custom Software Cost Estimator, use the MVP Scope Builder if the first release is still too broad, or contact us through the mobile app development service page for a reviewed roadmap.