Quick Answer: AI Compliance Automation for Banks

AI compliance automation for banks uses AI, workflow software, document processing, rules, integrations, and human-review queues to speed up regulated compliance work without handing final accountability to the model. The best use cases are support workflows around KYC intake, document extraction, sanctions and AML alert triage, policy Q&A, audit evidence collection, exception routing, and reporting preparation.

The practical rule is simple: AI can collect, classify, summarize, compare, recommend, and prepare evidence. Compliance officers, risk teams, and approved bank staff should retain ownership of regulated decisions, customer treatment, suspicious activity escalation, policy interpretation, and final approvals. This article is implementation guidance for software planning, not legal advice. Banks should validate any workflow with compliance counsel, model risk owners, information security, and applicable regulators.

Why Bank Compliance Automation Needs a Different Standard

Banking compliance workflows are not ordinary back-office automation. They touch customer identity, fraud exposure, sanctions screening, suspicious activity decisions, confidential records, audit evidence, third-party tools, and supervisory expectations. A generic AI assistant can create speed, but a regulated workflow needs traceability, role-based access, approved data sources, clear accountability, and evidence that the system behaves as intended.

Official guidance reinforces that context. FinCEN's customer identification guidance says a bank's Customer Identification Program is only one part of a broader BSA/AML compliance program and should be supported by risk-based verification procedures. FFIEC technology guidance keeps the operating model grounded in managed architecture, infrastructure, operations, resilience, and controlled delivery of critical financial services.

The 2026 model-risk update matters because it does not give banks a blank check for compliance AI. OCC Bulletin 2026-13 and Federal Reserve SR 26-2 modernize model-risk expectations around model use, validation, monitoring, governance, controls, and third-party considerations, while also saying generative and agentic AI are novel, rapidly evolving, and outside the scope of that specific guidance. A bank should therefore treat compliance AI assistants as governed technology and operational-risk systems even when a particular use case does not fit neatly inside one model-risk category.

COSO's 2026 generative AI control guidance adds a practical internal-control lens: maintain an inventory of AI use cases, assign clear owners and escalation paths, monitor controls continuously, and preserve traceability around inputs, outputs, model/configuration versions, and human review. In bank compliance workflows, this translates into reviewer-visible sources, immutable case logs, prompt/configuration change control, exception queues, and fallback procedures before scaling.

That means a bank should not start by asking, "Can AI replace compliance analysts?" A stronger question is: which compliance tasks are repetitive, evidence-heavy, and reviewable enough for AI to assist without weakening control?

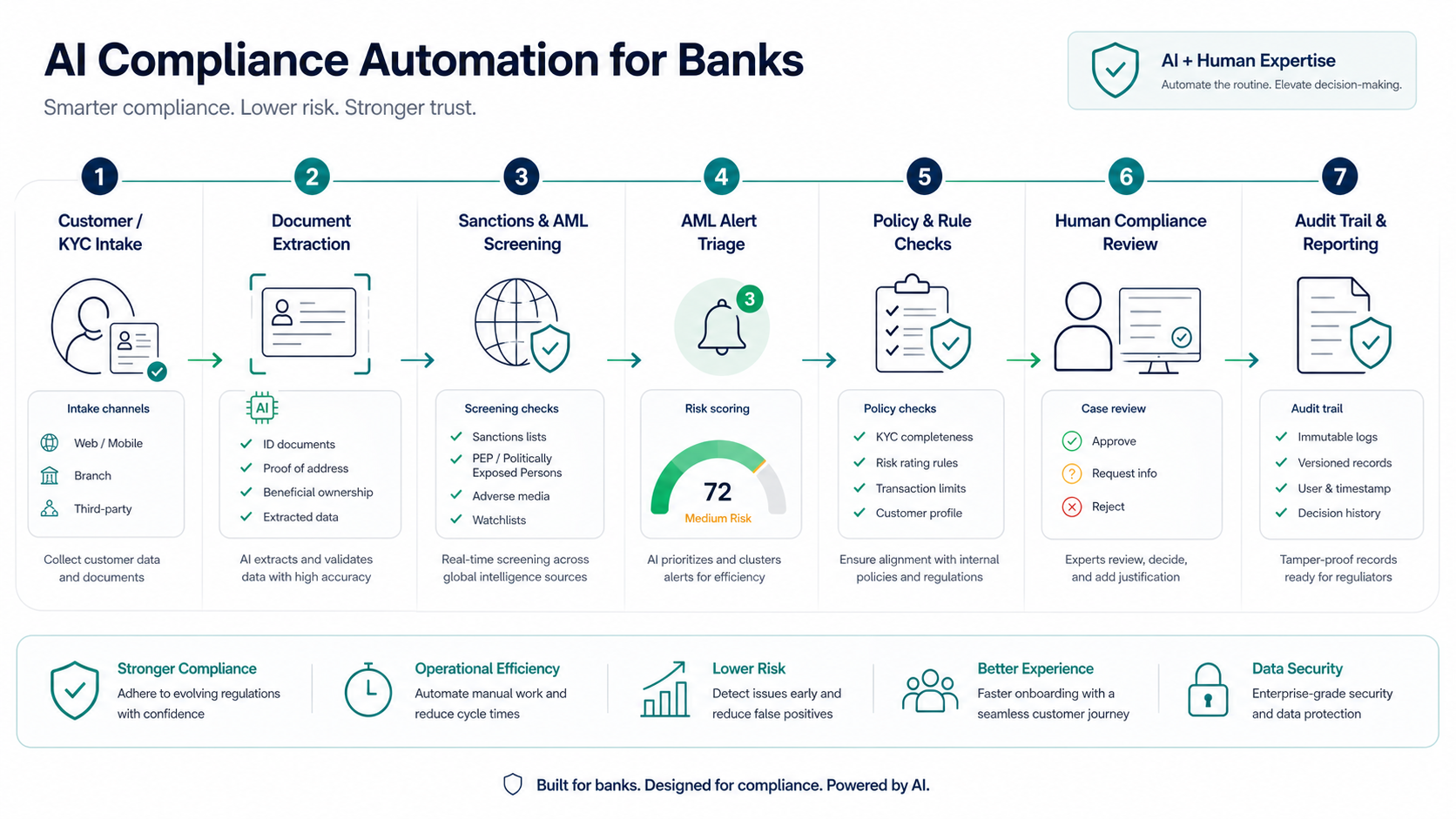

Where AI Can Safely Support Compliance Workflows

AI compliance automation creates value when it reduces manual handling around clearly bounded tasks. It is especially useful where teams repeatedly gather documents, compare fields, search policies, summarize case notes, route exceptions, or prepare evidence packs for review. These workflows are high-friction, but they are also measurable and auditable.

| Workflow | AI can assist with | Human should own |

|---|---|---|

| KYC intake | Extracting document data, checking missing fields, matching customer forms to checklist requirements | Final customer acceptance, exceptions, enhanced due diligence, and policy interpretation |

| AML alert triage | Summarizing transaction context, clustering related alerts, drafting investigation notes | Disposition, escalation, suspicious activity decisions, and regulatory filing choices |

| Sanctions review support | Organizing possible matches, collecting identifiers, highlighting conflicts in source records | True-match determination, customer communication, holds, and escalation |

| Policy Q&A | Retrieving approved policy passages and showing source references | Policy ownership, exceptions, interpretation, and updates |

| Audit evidence | Assembling logs, approvals, case notes, data lineage, and workflow history | Evidence acceptance, audit response, remediation commitments, and sign-off |

| Reporting prep | Drafting summaries, reconciling metrics, and identifying incomplete records | Submission, attestation, narrative approval, and regulator-facing statements |

For broader automation planning, NextPage's AI workflow automation ROI guide explains how to model human review, payback, integration cost, and risk controls across intake, retrieval, rules, approvals, and monitoring. Banking compliance is a stricter version of that architecture because the controls must be explicit from day one.

KYC and Customer Due Diligence Automation

KYC is a good starting point because the process has repeated inputs, clear document requirements, and visible handoff points. AI can extract names, addresses, date fields, identification numbers, beneficial ownership data, business descriptions, and missing-document signals from forms and uploaded files. It can also compare submitted records against the checklist that applies to the customer segment.

The system should not silently approve customers. A better pattern is to produce a review packet: extracted fields, confidence levels, source snippets, document quality flags, missing information, prior-account context where allowed, and exception notes. Reviewers can then approve, reject, request more information, or escalate enhanced due diligence with a complete audit trail.

This is where engineering detail matters. Identity-aware access, encryption, retention rules, redaction, queue design, and audit logs are as important as model quality. The cost drivers often resemble other regulated financial products, which is why the fintech app development cost guide is a useful companion when estimating integrations, security, compliance, and support work.

AML Alert Triage and Investigation Support

AML teams often face repeated alert review, noisy rules, fragmented records, and time-consuming case documentation. AI can help by summarizing transaction histories, grouping related alerts, extracting customer profile context, comparing case facts with approved typologies, and drafting investigation notes for human review.

Use AI here as an analyst assistant, not an autonomous compliance decision maker. It should show sources, separate facts from recommendations, surface uncertainty, and make escalation easy. Every AI-generated summary should remain editable and attributable. Analysts need to know which source systems and records informed the output.

For risk-scoring and anomaly-detection use cases, the strongest projects usually combine data engineering, measurement, validation, and governance. NextPage's machine learning for fintech fraud detection and credit risk guide explains when ML is appropriate for risk workflows and when rules, dashboards, or process cleanup should come first.

A Control Architecture for Bank AI Compliance

A bank compliance automation system should be designed around controls, not just prompts. The core architecture includes approved data sources, retrieval boundaries, policy versioning, permissions, model routing, confidence thresholds, case queues, human approval gates, immutable logs, monitoring, and rollback. Each workflow should document what the AI may do, what it may suggest, and what it may never finalize.

| Control layer | Design question | Evidence to keep |

|---|---|---|

| Data access | Which records can the AI read, and under which role? | Access policy, field map, data lineage, redaction rules |

| Knowledge sources | Which policy manuals, procedures, and checklists are approved? | Source inventory, version history, approval owner |

| Decision boundary | Which actions require human approval every time? | Workflow matrix, approval log, exception reasons |

| Model behavior | How are outputs tested, monitored, and challenged? | Test cases, defect logs, outcome monitoring, validation notes |

| Audit trail | Can the bank reconstruct what happened later? | Input references, prompts/configuration, generated output, reviewer action |

| Vendor and fallback | What happens if a vendor model changes or becomes unavailable? | Vendor diligence, SLAs, fallback process, contingency plan |

The secure AI agent development checklist is relevant when the automation can touch tools, private records, outbound messages, case systems, or regulated workflows. Permissions, audit logs, and tool boundaries should be implementation requirements, not launch-week additions.

Data Readiness Checklist

Most compliance AI projects fail on data and workflow readiness before they fail on model capability. Before building, map the source systems, document types, field quality, exception types, ownership, and approval paths. Then decide whether the first release should use document extraction, retrieval-augmented policy search, rules, classic ML, generative summaries, or an AI agent with tool access.

- Source ownership: each policy, checklist, transaction table, document store, and case system has a named owner.

- Data quality: critical fields are complete enough for reliable extraction, matching, filtering, and review.

- Version control: policies and procedures are versioned so the system can cite the right source.

- Access control: reviewers, analysts, managers, auditors, and admins have separate permissions.

- Exception taxonomy: the team knows which cases are routine, ambiguous, urgent, sensitive, or prohibited for automation.

- Outcome labels: the team can measure false positives, missed issues, rework, reviewer overrides, and escalation quality.

- Retention rules: logs, generated summaries, and source references follow bank retention and privacy requirements.

If the team is unsure where to start, NextPage's AI Agent Readiness Assessment can help score workflow clarity, data readiness, integration access, and human-review controls before the bank commits to a production build.

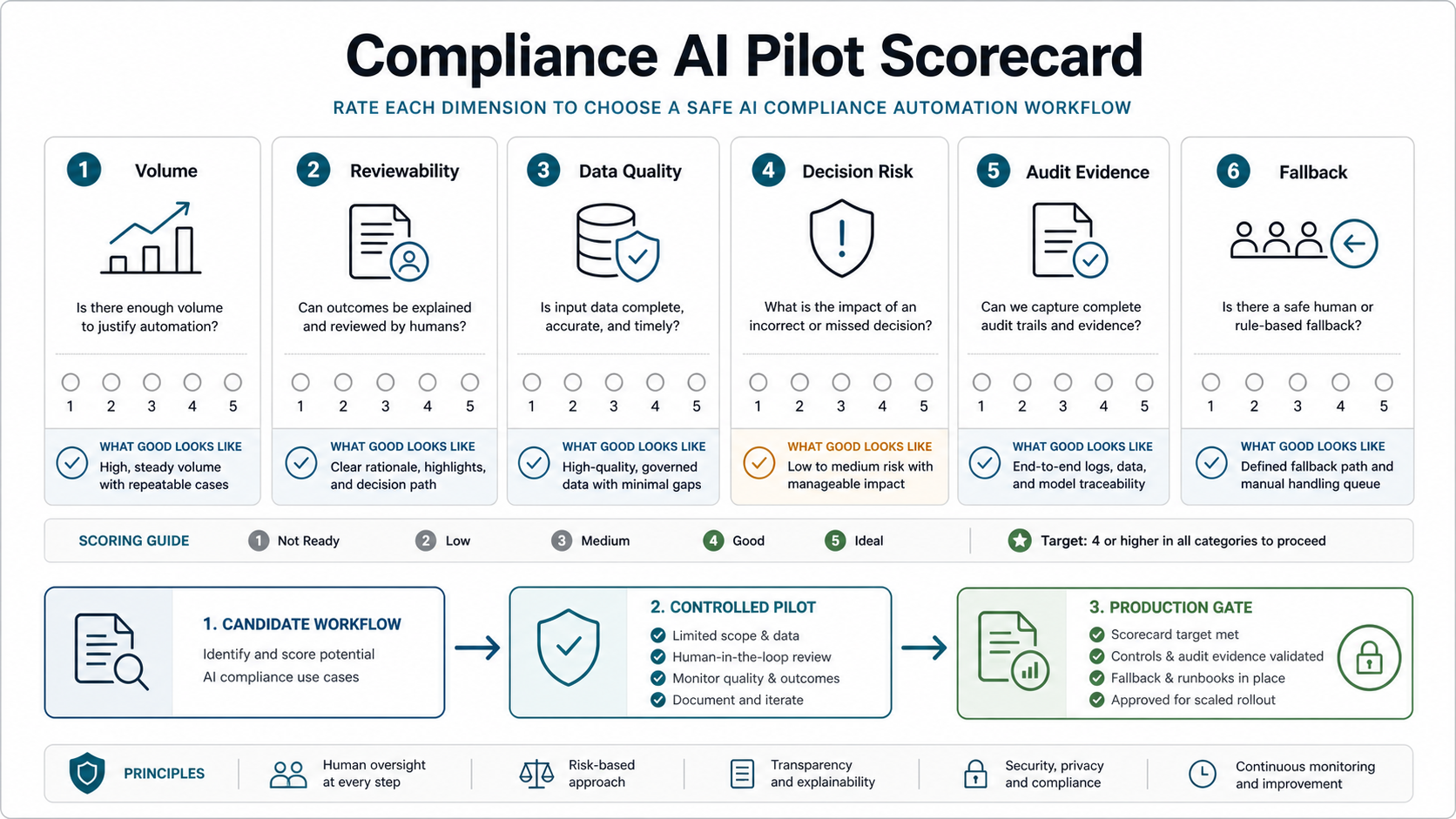

Pilot Scorecard For Bank Compliance AI

Before choosing the first workflow, score each candidate against six practical questions. The safest pilots are high-volume, evidence-heavy, reviewable, and reversible. The riskiest pilots combine unclear data, high customer impact, weak audit evidence, and no fallback path.

| Scorecard factor | Green-light signal | Red flag |

|---|---|---|

| Volume | The task repeats often enough to measure time saved and quality change. | The workflow is rare, bespoke, or mostly judgment-based. |

| Reviewability | A human reviewer can inspect sources and approve, reject, or correct output quickly. | Reviewers cannot see why the AI produced an answer. |

| Data quality | Required documents, fields, policies, and case records are complete and versioned. | Key evidence lives in emails, screenshots, or inconsistent free text. |

| Decision risk | The AI prepares evidence or recommendations; it does not finalize customer outcomes. | The workflow could silently approve, deny, block, or report without a gate. |

| Audit evidence | The system can retain inputs, sources, prompts/configuration, output, reviewer action, and timestamps. | The team cannot reconstruct what happened later. |

| Fallback | The bank can route work back to the existing process if the model, vendor, or integration fails. | There is no manual route or operating procedure for service disruption. |

Acceptance Gates Before Scaling Compliance AI

A pilot is not ready to scale just because reviewers like the interface or early cases look accurate. Banks should define acceptance gates before the pilot starts, then require evidence from production-like cases before expanding into higher-risk queues. The gate should be signed off by compliance, model risk or AI governance, information security, operations, legal where needed, and the business owner who will live with the workflow.

| Gate | Evidence to collect | Scale decision |

|---|---|---|

| Purpose and risk boundary | Approved use-case inventory, prohibited actions, customer-impact classification, and human decision owner | Scale only if the AI supports work rather than silently approving, denying, reporting, or escalating customers. |

| Data and source control | Versioned policies, document sources, data lineage, retention rules, and access controls | Scale only if reviewers can see the source record and stale or missing evidence is routed to exception handling. |

| Validation and challenge | Representative test set, false-positive and false-negative review, edge cases, override analysis, and bias checks | Scale only if error patterns are understood and the team has a remediation backlog with owners. |

| Human-review evidence | Reviewer action, rationale, timestamp, queue status, escalation path, and final sign-off logs | Scale only if the audit trail proves who made the regulated decision and what evidence they saw. |

| Monitoring and fallback | Quality metrics, drift signals, vendor/integration status, incident triggers, and manual operating procedure | Scale only if the bank can pause the AI path and keep compliance work moving without data loss. |

This gate turns AI compliance automation from a demo into an operating-control decision. It also gives internal audit and technology risk teams a concrete evidence pack to review before the workflow becomes part of daily KYC, AML, sanctions, reporting, or audit-response operations.

Implementation Roadmap

Start with one bounded workflow where the current baseline is measurable. KYC document completeness, policy Q&A with citations, alert summarization, and audit evidence assembly are usually safer pilots than autonomous account decisions or customer-facing compliance advice. The first release should prove quality, reviewer trust, and auditability before expanding to more sensitive steps.

| Phase | Goal | Output |

|---|---|---|

| 1. Workflow selection | Choose a repeatable, reviewable compliance task with enough volume | Use-case scorecard and risk boundary |

| 2. Control design | Define data sources, permissions, approval gates, and logging | Control matrix and operating procedure |

| 3. Prototype | Build extraction, retrieval, summary, or triage support for one queue | Reviewer-facing pilot with source citations |

| 4. Validation | Test accuracy, completeness, bias, false positives, overrides, and audit trail quality | Validation report and defect backlog |

| 5. Production rollout | Integrate with case systems, monitoring, reviewer queues, and support process | Controlled release with metrics and rollback |

| 6. Expansion | Add new workflows only after evidence shows quality and control | Roadmap by compliance value and risk |

Commercially, the first business case should combine effort saved, review quality, turnaround time, audit-readiness improvements, and rework reduction. The Workflow Automation Opportunity Finder can help shortlist candidate queues, and the AI Automation ROI Calculator can quantify hours saved from repeated operational work before the team builds a detailed compliance-specific ROI model.

What to Avoid

The riskiest projects try to automate the highest-stakes decision before the bank has clean data, policy ownership, reviewer trust, or monitoring. Avoid black-box customer approval, unsupported policy answers, unlogged AI recommendations, broad tool permissions, unclear vendor dependencies, and dashboards that only show speed while hiding overrides and defects.

Also avoid treating AI outputs as neutral. Compliance teams should test representative cases, edge cases, adverse outcomes, stale policy sources, incomplete documents, and ambiguous customer records. Reviewers should be able to challenge, correct, and improve the system without losing the record of what happened.

NextPage's AI governance for critical infrastructure software guide goes deeper on owners, permissions, human review, monitoring, and rollback for regulated and high-impact systems. Those controls are especially important when a banking AI workflow moves from analysis into tool-assisted action.

Build vs Buy for Bank Compliance AI

Banks do not need custom software for every compliance task. A vendor platform may be right when the workflow is standardized, integrations are supported, evidence requirements fit the product, and the bank can validate the vendor's outputs and limitations. Custom software makes more sense when workflows are proprietary, multiple systems must be joined, reviewers need a tailored queue, policies are bank-specific, or the experience must fit existing operations.

A practical approach is often hybrid: buy or integrate specialized identity, screening, case management, or monitoring tools, then build the orchestration layer that connects internal data, reviewer workflows, audit evidence, and management reporting. For AI workflows that need financial-services controls from the start, NextPage's AI agents for banking and finance workflows service page shows how governed agents can be scoped around approvals, permissions, audit trails, and controlled tool access. NextPage's custom software development work fits that middle layer when the bank needs reliable workflow delivery around existing systems.

Budget depends on integrations, data cleanup, permissions, validation, reporting, and support. The custom software development cost guide can help frame those drivers before scoping a bank-specific compliance automation project.

When NextPage Can Help

NextPage helps teams turn AI compliance automation ideas into buildable workflow plans. We start by mapping the current process, risk boundaries, source systems, reviewer roles, and evidence requirements. Then we design the right mix of rules, retrieval, intelligent document processing, AI summaries, dashboards, audit logs, and human approval gates.

If your bank, fintech, or lending team is evaluating AI for KYC, AML support, document review, policy search, audit evidence, or reporting preparation, start with a narrow pilot and a control matrix. NextPage can help run a banking AI compliance workflow assessment, estimate implementation effort, and build a production path through AI development services and banking-specific AI agent delivery that keep compliance ownership, human review, and auditability intact.