Quick Answer: What Architecture Should A Cash-In/Cash-Out Wallet Use?

A cash-in/cash-out wallet should treat the mobile app as only one surface in a larger money-movement system. The reliable architecture has five parts: a user app, an agent or merchant app, an orchestration API, an append-only wallet ledger, and an operations layer for limits, KYC/AML checks, settlement, and reconciliation.

The most important decision is to make the ledger the source of truth. A deposit should not simply add a number to a wallet balance, and a withdrawal should not only subtract one. Each event needs a verified request, an idempotency key, a double-entry posting, agent float checks, a receipt, and reconciliation against cash, bank, or settlement records. That is what keeps the product auditable when agents, users, currencies, fees, and failed requests multiply.

For an MVP, keep the first release narrow: one user wallet, one agent role, one currency or market, QR-based request validation, transaction limits, manual exception review, admin reconciliation, and clear support workflows. Use the MVP Scope Builder to separate the release-one workflow from later ideas such as multi-currency exchange, agent commissions, dynamic liquidity routing, and automated risk scoring.

What Cash-In And Cash-Out Mean In A Wallet Product

Cash-in lets a customer load value into a digital wallet by handing physical cash to an approved agent, merchant, money changer, branch, or field operator. Cash-out does the opposite: the customer requests a withdrawal in the app and receives physical cash from an approved cash point after the request is validated.

The workflow is common in remittance apps, local money-transfer products, neobanking pilots, stored-value wallets, market-specific payment apps, and fintech products that serve users who still need a bridge between cash and digital value. It can also appear in currency exchange app development and digital currency products where a customer exchanges value digitally but collects or deposits fiat through verified local operators.

The source case study behind this queue item describes a currency exchange platform where users could deposit or withdraw fiat at verified money changer locations, validate the request through generated QR receipts, and rely on a secure backend for account and transaction handling. That is a useful starting point, but a production-ready buyer needs a clearer implementation model than a case study can provide.

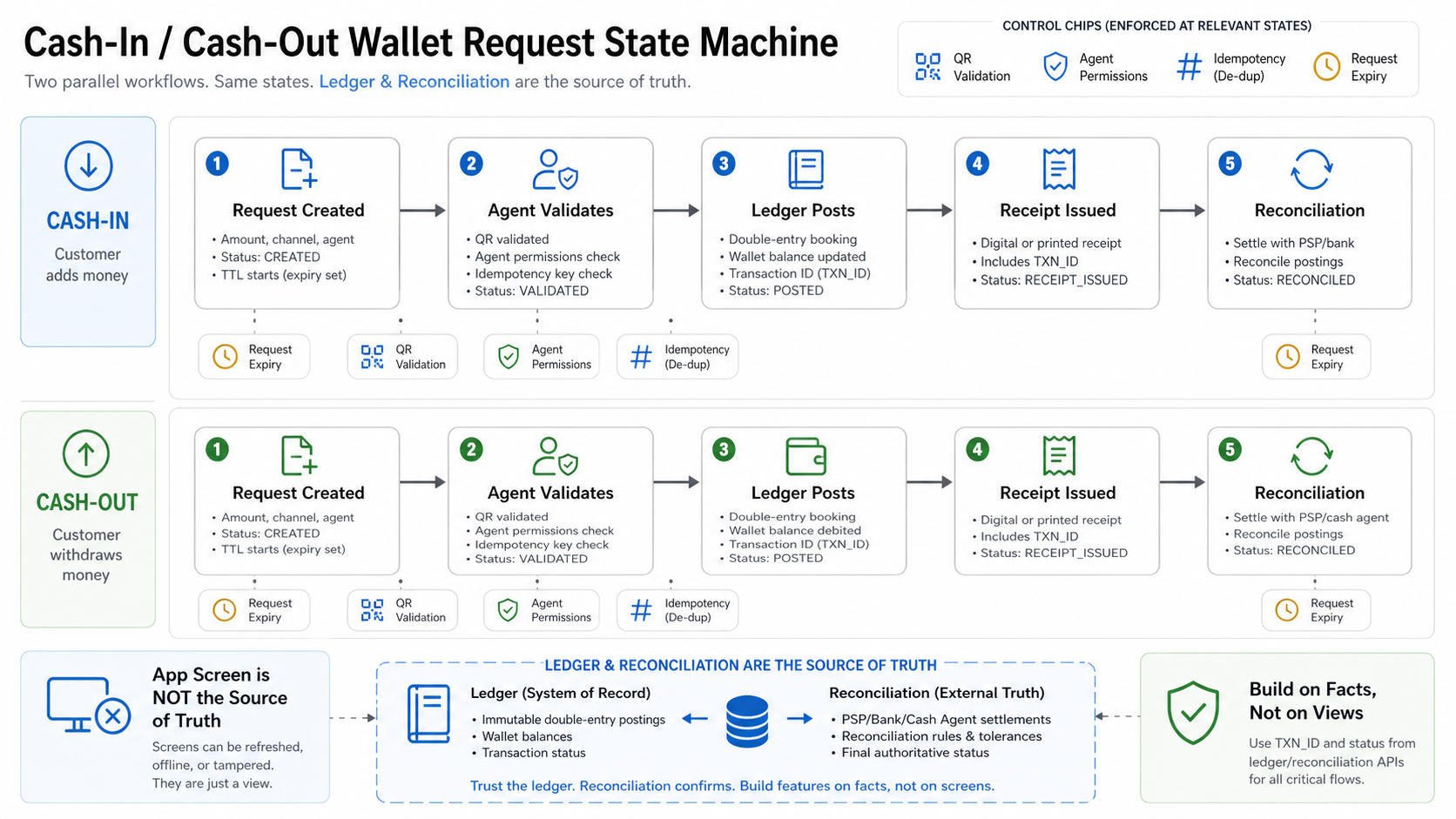

The Cash-In Flow

A cash-in flow starts when the user wants to convert physical cash into wallet balance. The user creates a deposit request in the app, chooses or confirms the agent location, and receives a request reference or QR code. The agent scans or enters the request, verifies identity and amount, accepts cash, and confirms the transaction. The backend posts the ledger event and the user sees the updated wallet balance.

The system should not credit the wallet just because the agent taps confirm. It should validate the request state, agent permissions, agent float or till rules, amount limits, idempotency key, risk flags, and any market-specific KYC requirements before posting. If the same QR code is scanned twice, the second attempt should be rejected or treated as a duplicate, not posted again.

| Step | System Responsibility | Risk To Control |

|---|---|---|

| User creates deposit request | Generate reference, amount, expiry, and QR payload | Fake receipts or stale requests |

| Agent validates request | Check agent role, location, amount, user identity, and request state | Unauthorized cash point or social engineering |

| Cash is accepted | Record agent confirmation, receipt, timestamp, and device context | Disputes over whether cash changed hands |

| Ledger is posted | Credit user wallet and debit cash-in clearing or agent float account | Balance drift, duplicate posting, missing audit trail |

| Reconciliation runs | Compare ledger, agent cash reports, settlement records, and exceptions | Leakage, fraud, unresolved variances |

The Cash-Out Flow

A cash-out flow is more sensitive because the system releases physical cash. The user creates a withdrawal request, the backend reserves or debits wallet value according to the product rules, and the agent pays cash only after the request is validated. The flow must handle expiration, cancellation, partial failures, insufficient agent cash, failed scans, and user disputes.

The cleanest MVP pattern is to move the wallet balance into a pending withdrawal state before the agent pays cash. After the agent confirms payout, the ledger finalizes the withdrawal and records the agent-side entry. If the request expires or is cancelled before payout, the system reverses the pending state with a linked reversal entry. Avoid silent balance edits.

| Failure Case | Recommended Handling | Evidence Needed |

|---|---|---|

| User requests cash but agent has no liquidity | Cancel, reroute, or keep pending until expiry | Agent cash status and cancellation reason |

| QR is scanned twice | Use idempotency and request state to block duplicate payout | Original transaction ID and scan history |

| User disputes cash receipt | Review receipt, agent confirmation, device, timestamp, and support notes | Audit trail and payout acknowledgment |

| Network drops after confirmation | Retry idempotently and reconcile final state | Request ID, idempotency key, and ledger status |

| Risk rule blocks payout | Hold for review or ask for additional verification | Rule ID, reviewer action, and customer communication |

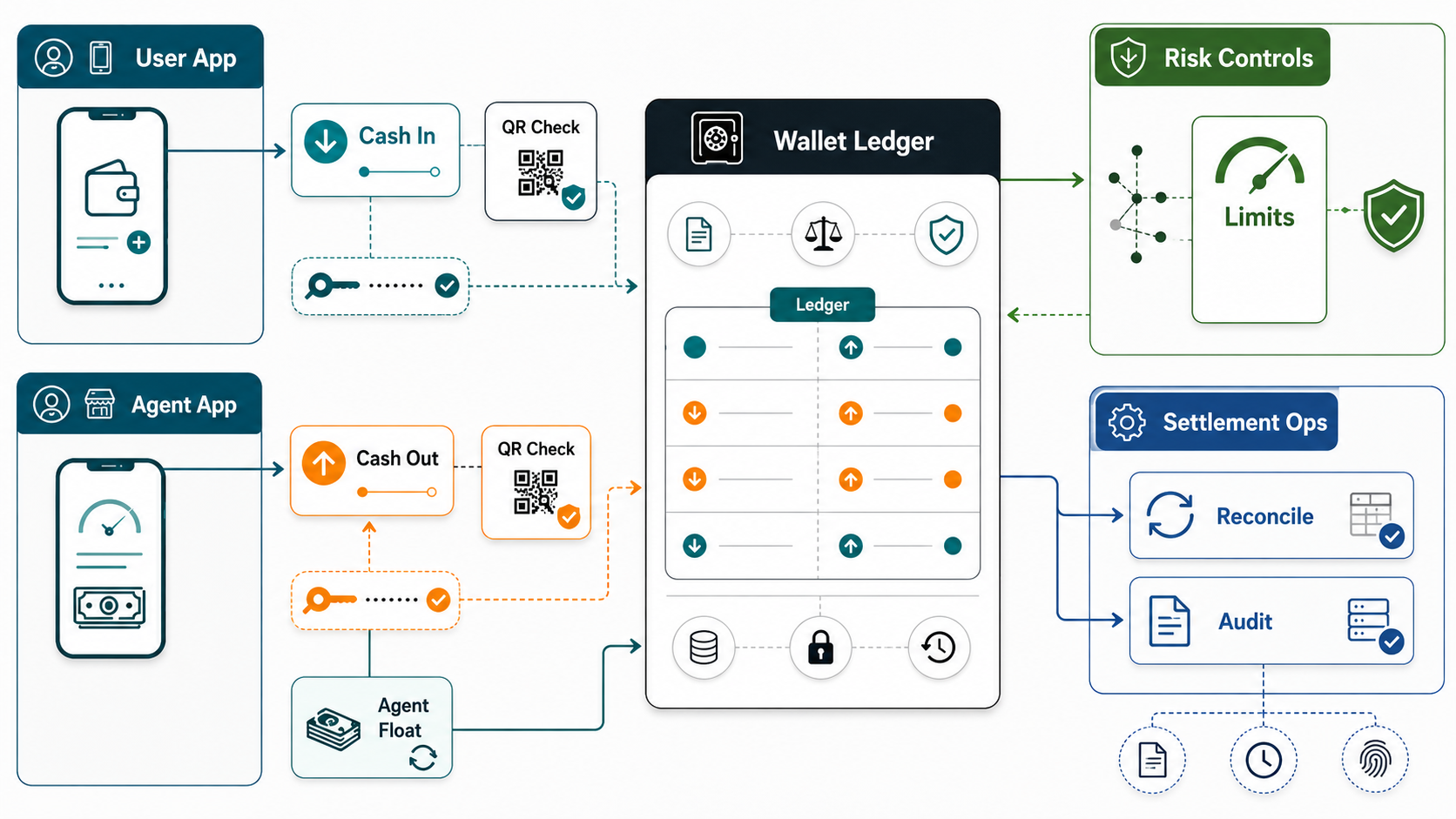

Core Architecture Layers

A cash-in/cash-out wallet combines mobile UX, backend workflow, compliance, and operations. The architecture should be designed as a money system, not a normal CRUD app.

- User app: wallet balance, deposit request, withdrawal request, QR receipt, transaction history, support status, and notification flow.

- Agent app: request scan, amount confirmation, cash-in/cash-out actions, agent float view, customer verification prompts, receipt generation, and end-of-day summary.

- Backend orchestration API: request lifecycle, state machine, idempotency, permissions, device context, notifications, and exception handling. NextPage's backend and API development services are relevant when this layer needs reliable transaction boundaries and integration design.

- Wallet ledger: append-only journal entries, account hierarchy, fees, reversals, holds, settlements, and balance projections.

- Risk and compliance layer: KYC status, transaction limits, velocity checks, suspicious-pattern alerts, agent risk, AML review queues, sanctions or watchlist integrations where required, and audit evidence.

- Operations console: agent onboarding, liquidity monitoring, reconciliation, disputes, settlement batches, manual review, and reporting.

If you are planning the broader product, start from eWallet app development services rather than isolated screens. Wallet products need product design, ledger thinking, secure backend engineering, QA, DevOps, and operational controls to work together.

Design The Wallet Ledger Before The Screens

The wallet ledger is the system of record for money movement. Every wallet transaction should be traceable to one or more immutable ledger entries that balance. A cash-in may credit the user wallet and debit an agent cash-in clearing account. A cash-out may debit the user wallet and credit an agent payout or cash-out clearing account. Fees, reversals, commissions, settlement adjustments, and failed transactions should be linked events, not manual balance edits.

| Ledger Event | Debit | Credit | Why It Matters |

|---|---|---|---|

| Cash-in confirmed | Agent cash-in clearing | User wallet | User receives digital value backed by accepted cash |

| Cash-out requested | User wallet or available balance | Pending withdrawal | Funds are reserved before cash is released |

| Cash-out paid | Pending withdrawal | Agent payout clearing | Physical cash payout is finalized |

| Request expired | Pending withdrawal reversal | User wallet | Funds are restored with an audit trail |

| Agent commission | Fee expense or customer fee | Agent commission payable | Agent incentives stay reconcilable |

Use idempotency keys for every operation that could be retried. Store external references, QR payload identifiers, device context, actor IDs, timestamps, and request state transitions. Reconciliation is much easier when the system can answer who initiated the request, who validated it, what ledger entries were posted, whether they balanced, and what changed after support or operations intervened.

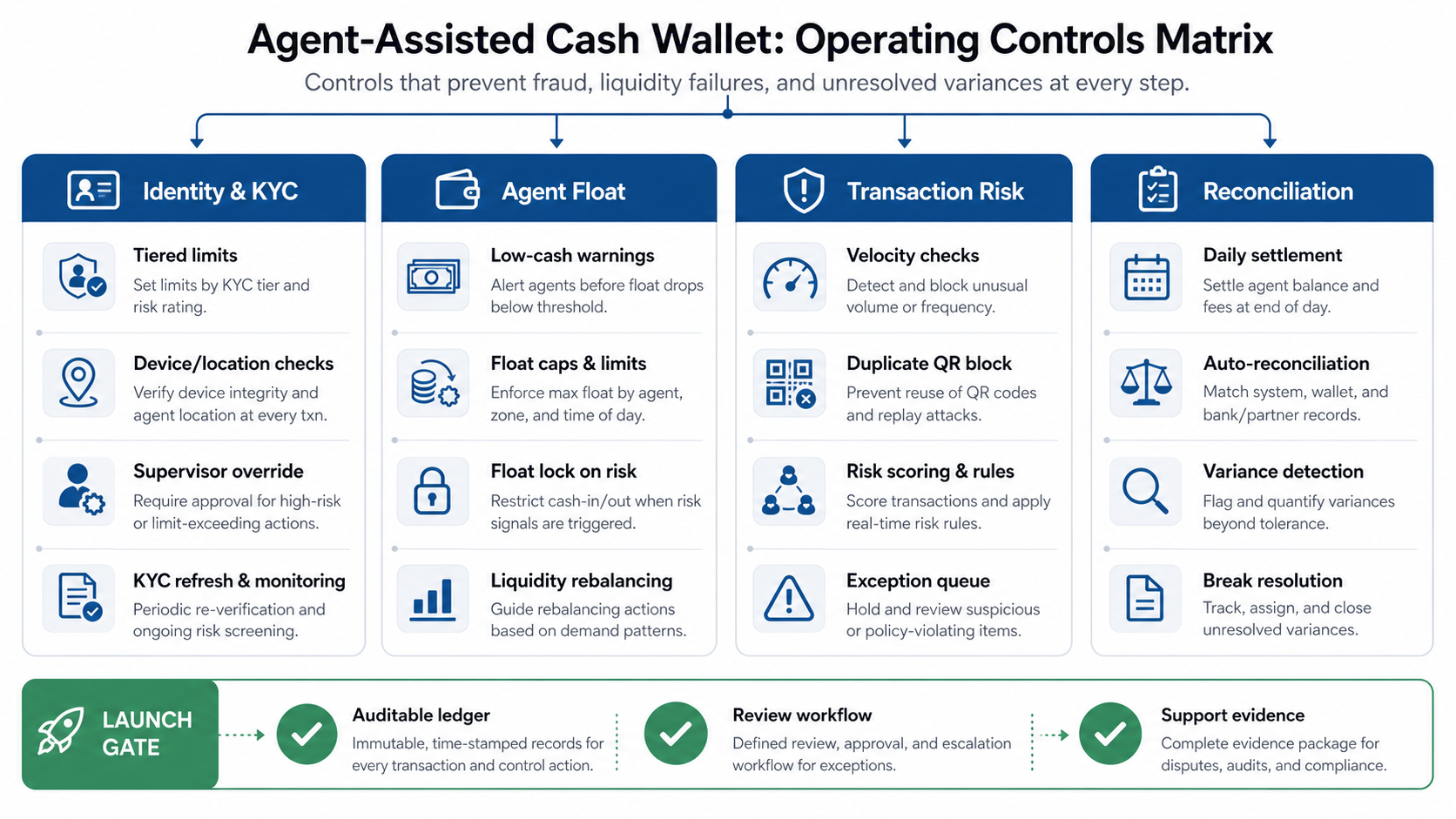

Agent Float And Liquidity Controls

Agent-assisted wallets fail operationally when agent liquidity is treated as an afterthought. For cash-in, the agent may need a way to report accepted cash and settle it with the operator. For cash-out, the agent needs enough physical cash to pay the customer. The system should track agent float, daily limits, pending requests, unsettled balances, and reconciliation status.

The MVP does not need advanced liquidity optimization, but it does need boundaries. Set per-agent and per-user transaction limits, require supervisor approval for unusual amounts, show low-cash warnings, and prevent an agent from confirming a payout that their configured cash position cannot support. If the product operates across currencies or locations, model each currency and settlement location explicitly.

Risk, KYC, AML, And Fraud Controls

Cash-in/cash-out workflows are fraud-sensitive because they connect digital balances with physical cash. A normal app login is not enough. The product should know the user, the agent, the device, the location context, the amount, the request pattern, and the history of both parties.

| Control | MVP Version | Later Version |

|---|---|---|

| KYC gating | Require verified profile before higher limits | Tiered KYC with market-specific rules |

| Transaction limits | Daily and per-transaction caps | Dynamic limits by risk, user age, agent score, and geography |

| QR validation | Signed, expiring request payload | Device binding, geofencing, and stronger proof-of-presence |

| Velocity checks | Flag repeated attempts and rapid reversals | Risk scoring and automated case creation |

| Agent controls | Role permissions and supervisor override | Agent scorecards, liquidity forecasting, and anomaly detection |

Compliance requirements vary by market and product model, so this article should not be treated as legal advice. The engineering takeaway is still consistent: build auditability, controls, review queues, and reporting hooks early. Retrofitting them after launch is slower and more expensive than including a practical baseline in the first release.

What Belongs In The MVP?

A strong MVP proves that users and agents can complete the cash bridge safely. It should not try to launch every currency, settlement method, agent commission model, and compliance automation at once.

| Include In Release One | Usually Later |

|---|---|

| One market or operating model | Multi-country rollout |

| User wallet, agent app, admin console | Advanced agent network marketplace |

| Cash-in and cash-out request state machine | Dynamic routing across agents |

| QR validation, expiry, duplicate protection | Biometric or NFC proof flows |

| Basic KYC gates and transaction limits | Automated AML case intelligence |

| Append-only ledger and manual reconciliation | Fully automated settlement optimization |

| Receipts, notifications, and support trail | Advanced loyalty, rewards, and promotions |

Use FinTech app development cost planning to estimate the release by workflow risk, not just by screen count. The expensive parts are usually ledger design, security, compliance evidence, integrations, reconciliation, QA, and production operations.

Cost Drivers And Team Shape

Cash-in/cash-out wallet cost depends on how many roles, currencies, integrations, compliance gates, and exception workflows the first release needs. A basic pilot with one market and manual reconciliation is very different from a multi-currency wallet with agent settlement, exchange rates, automated AML review, and third-party banking integrations.

| Driver | Why It Changes Scope |

|---|---|

| Ledger complexity | Holds, reversals, commissions, fees, and settlements require more design and tests |

| Agent network model | Onboarding, permissions, float, cash reports, and disputes add admin workflows |

| Compliance requirements | KYC, AML, limits, reporting, and audit trails vary by market |

| Integrations | Identity, notifications, payment rails, banking, FX, and analytics require resilient APIs |

| Reconciliation depth | Manual exports are simpler than automated settlement matching and exception queues |

| Availability and support | Money products need stronger logging, monitoring, QA, and incident response |

The Custom Software Cost Estimator can help turn these drivers into a directional range. For deeper planning, compare the wallet against broader custom software development cost drivers such as user roles, workflow complexity, integrations, security, and operational risk.

Build Checklist Before You Hire A Team

Before choosing a development partner, ask for evidence that they understand money movement, not just mobile UI. A credible team should be able to explain ledger design, duplicate prevention, auditability, agent operations, reconciliation, and secure release practices.

- What is the source of truth for wallet balance?

- How are cash-in and cash-out requests represented as states?

- How does the system prevent duplicate QR scans and duplicate ledger postings?

- How are agent float, limits, and settlement records modeled?

- What happens when a request is confirmed but the network drops?

- Which events can be reversed, and how are reversals linked to original entries?

- What data is available for support and compliance review?

- How are production incidents, suspicious transactions, and reconciliation variances handled?

These questions overlap with a broader custom software development company checklist, but wallet projects deserve extra scrutiny because the product handles value, trust, and operational liability.

NextPage's Practical Recommendation

For most FinTech founders, the safest path is to start with a narrow, auditable wallet MVP. Build one cash-in flow, one cash-out flow, one agent model, one ledger model, and one reconciliation workflow before scaling to more markets or financial products. Keep compliance and legal advisors involved for market-specific obligations, but make sure the engineering architecture can produce the evidence they will ask for.

NextPage can help plan and build this kind of product through eWallet app development services, backend/API architecture, mobile app development, and MVP scoping. The goal is not to ship a flashy wallet interface first. The goal is to ship a product where every cash request, ledger entry, agent action, receipt, and exception can be explained.

Final Takeaway

Cash-in/cash-out wallet workflows succeed when product, engineering, compliance, and operations are designed together. The app needs a clean user experience, but the business depends on the ledger, agent controls, QR validation, limits, reconciliation, and audit trail behind it.

If you are planning a wallet MVP, start by mapping the money movement. Define who holds cash, who can approve a transaction, when the wallet balance changes, how failed requests are reversed, and how operations will reconcile the day. Once those answers are clear, the app scope, backend design, and build estimate become much more reliable.