A mobile banking app modernization roadmap should start with trust, not with a redesign wishlist. Banks, NBFCs, and fintech teams usually modernize because the current app is slow, hard to change, weak on security evidence, dependent on brittle core-banking APIs, or unable to support new onboarding, payments, cards, fraud, and servicing workflows.

The safest roadmap upgrades the customer experience and the underlying delivery system together. A polished app UI will not fix batch APIs, fragile authentication, missing consent records, poor observability, or release testing gaps. The modernization plan should connect mobile UX, identity, API architecture, compliance evidence, security testing, accessibility, analytics, and rollout controls into one program.

If the app is already live, treat the work as legacy software modernization and mobile product engineering, not a greenfield build. The goal is to improve trust and velocity without breaking account access, payments, customer support, or regulatory evidence.

Quick Answer: Mobile Banking App Modernization Roadmap

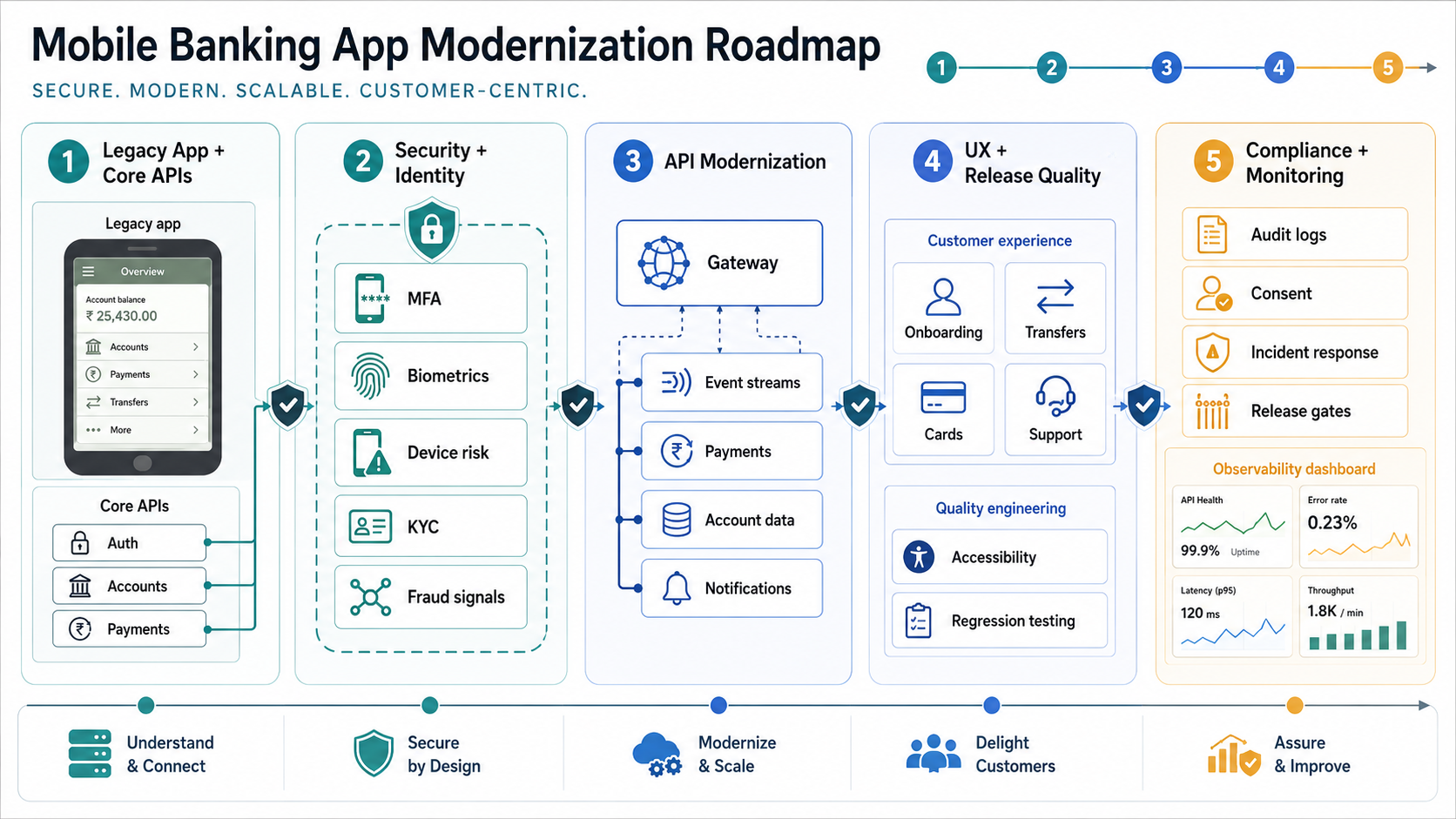

A practical mobile banking app modernization roadmap has six stages: assess the current app and risk surface, stabilize identity and security, modernize core banking and payment APIs, redesign the highest-friction journeys, build compliance and audit evidence into the workflow, then roll out through controlled pilots and regression gates. The work should preserve service continuity while improving speed, accessibility, fraud controls, and release confidence.

| Stage | Decision | Proof Needed |

|---|---|---|

| Assessment | Which journeys and systems create the biggest risk? | Crash, latency, support, fraud, API, and compliance evidence. |

| Identity | How will users authenticate and recover safely? | MFA, biometrics, device risk, KYC, consent, and recovery flows. |

| API upgrade | Which core, payment, card, notification, and data APIs must change? | Contracts, latency targets, fallback behavior, and audit logs. |

| UX rebuild | Which journeys must become simpler first? | Onboarding, balance, transfer, bill pay, card controls, support, accessibility. |

| Compliance | What evidence is needed for every regulated action? | Consent, KYC/AML status, fraud signals, release approvals, retention rules. |

| Rollout | How will the release expand safely? | Feature flags, beta cohorts, regression tests, monitoring, rollback. |

Modernization Is Different From Building A New Banking App

A new mobile banking app can define its architecture from the start. Modernization inherits customers, app-store ratings, support history, security controls, vendor contracts, core-banking constraints, and live transaction risk. That changes the plan. The team must protect existing users while replacing weak parts of the product.

The first step is a factual assessment. Review app crashes, slow screens, login failures, transaction drop-offs, fraud incidents, support tickets, accessibility gaps, dependency versions, API latency, release rollback time, audit findings, and security-test results. Map each issue to a business journey such as onboarding, account overview, transfers, card controls, bill pay, loan servicing, customer support, and notifications.

For teams planning a broader product rebuild, NextPage's mobile app development work covers mobile architecture, release planning, analytics, QA, and app-store readiness, while modernization adds migration and risk-control discipline.

Security And Identity Come Before Feature Expansion

Mobile banking modernization should harden identity before adding new customer journeys. Risk-based authentication, MFA, biometrics, device binding, session controls, step-up authentication, fraud signals, and secure account recovery all affect trust. Weak recovery flows can undo strong login controls, especially when customers lose devices or change phone numbers.

KYC and AML workflows also need modernization when onboarding moves faster. A strong app should collect identity evidence, show status clearly, route exceptions, store consent, and preserve audit trails. Fraud teams need signals from device, behavior, transaction context, account history, and support interactions without turning every customer action into friction.

Security work should include mobile app security hardening, API authorization, secrets handling, logging review, dependency scanning, penetration testing, and abuse-case testing. Use OWASP MASVS as the mobile verification baseline, align identity decisions with current NIST digital identity guidance, and pair the roadmap with security testing services before expanding high-risk transaction features.

Modernize APIs Around Real Banking Journeys

Many mobile banking problems are API problems wearing a UI mask. The app may wait on batch core systems, inconsistent customer data, slow payment rails, fragile card controls, manual KYC checks, or notification services that do not expose useful status. Modernization should define API contracts around journeys, not around whichever backend endpoint already exists.

Start with the highest-value paths: login, account summary, transaction history, transfer, bill payment, card freeze, beneficiary management, loan payment, dispute, support ticket, and notification preferences. For each path, define data owner, latency target, idempotency, error behavior, audit event, permission rule, and fallback state.

NextPage's API development roadmap is useful when the app needs an API gateway, event layer, versioned contracts, observability, and safer integration with legacy systems. Banking APIs should be designed for correctness and traceability before speed alone; performance-sensitive journeys should also use the release checks in the mobile app performance optimization checklist.

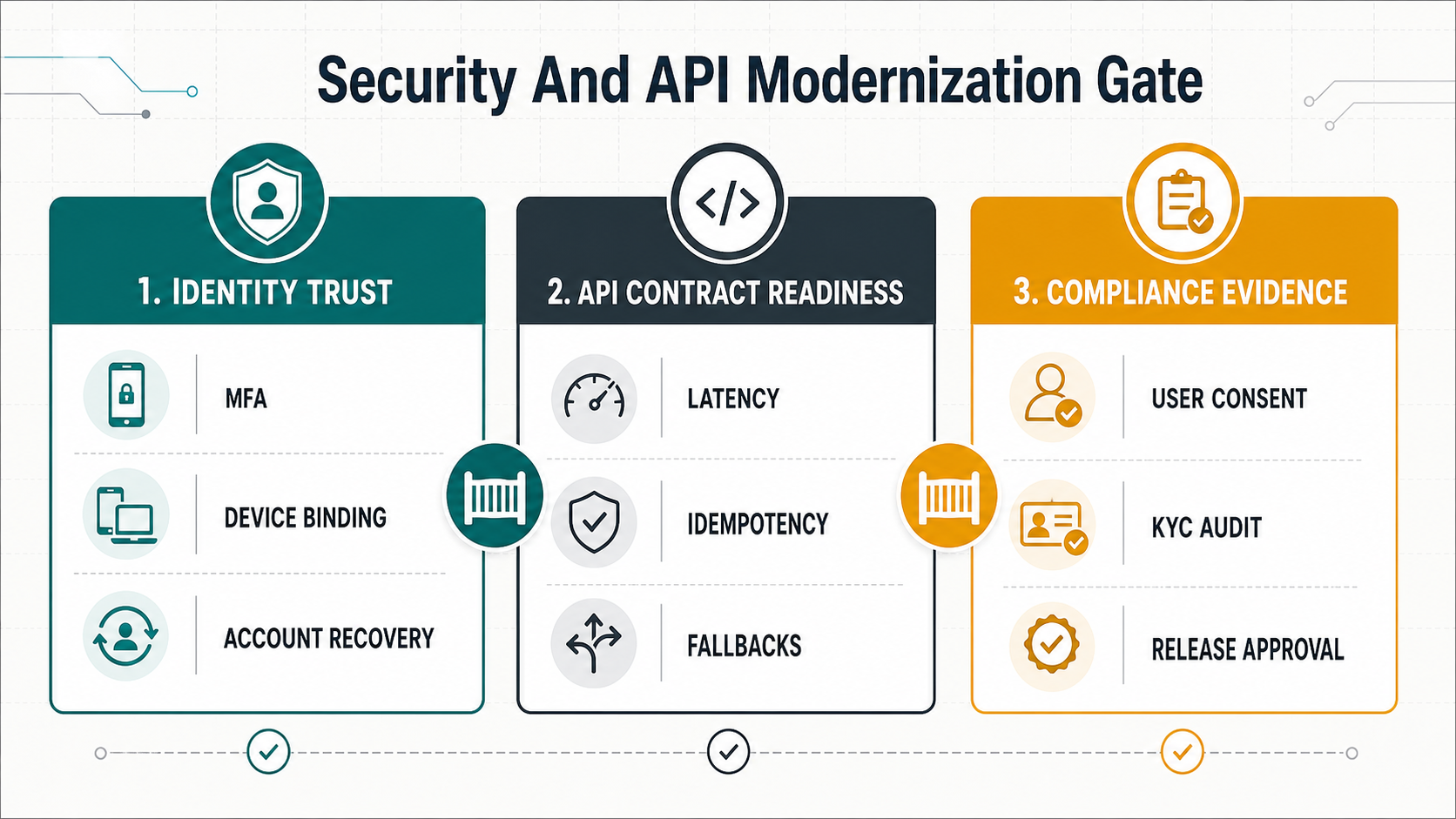

Add A Modernization Evidence Gate Before Each Release Wave

A banking modernization release should not move forward because a sprint is complete. It should move forward because the product team can show evidence across identity, APIs, compliance, support readiness, and rollback. This gate converts a large modernization program into smaller release decisions that product, engineering, security, compliance, and operations can review together.

| Gate | Minimum Evidence | Decision |

|---|---|---|

| Identity trust | MFA, device binding, recovery, session timeout, and step-up flows tested on real device classes. | Proceed only when risky journeys have recovery and support paths. |

| API readiness | Contracts, idempotency, latency budgets, audit events, and fallback states proven for each journey. | Hold journeys with ambiguous errors or duplicate-transaction risk. |

| Compliance proof | Consent, KYC/AML status, payment authorization, retention, and approval evidence captured without sensitive log leakage. | Proceed when evidence can support audit and customer support. |

| Release resilience | Regression, performance, security, monitoring, feature flags, and rollback have named owners. | Expand the cohort, pause, or roll back based on measured thresholds. |

Upgrade UX, Accessibility, And Release Quality Together

Mobile banking UX is not only visual design. It is whether customers can complete sensitive tasks without confusion: open an account, verify identity, understand balances, transfer money, manage cards, find statements, dispute a transaction, contact support, and recover access. Each journey should expose clear states, confirmation screens, error messages, support paths, and accessibility behavior.

Accessibility matters because banking is an essential service. Modernization should test screen-reader labels, focus order, color contrast, dynamic text, input errors, language clarity, and device compatibility. These checks belong in the release process, not only in final design review.

Use mobile app testing services to validate regression coverage across devices, OS versions, network conditions, authentication flows, payment paths, and accessibility states. A supporting functional testing checklist for web and mobile apps can keep journey coverage visible when modernization work spans app, API, admin, and support teams. Banking apps need repeatable evidence before every major rollout.

Build Compliance Evidence Into The Product

Compliance evidence should be generated by the workflow itself. When a user consents, verifies identity, changes device, adds a beneficiary, makes a transfer, updates contact details, requests support, or disputes a transaction, the system should preserve the right evidence without leaking sensitive data into logs.

Define audit events before implementation. Each regulated action should capture who initiated it, what system processed it, which policy applied, what decision was made, which exception path was used, and how long the record is retained. Product, compliance, security, and support teams should agree on what evidence is needed before the build starts.

| Evidence Area | What To Capture | Failure To Avoid |

|---|---|---|

| Consent | Purpose, timestamp, version, channel, withdrawal path. | Terms shown but not provable later. |

| KYC/AML | Status, provider result, review queue, exception reason. | Manual overrides with no audit trail. |

| Payments | Request, authorization, idempotency key, result, reversal path. | Duplicate transfer or unclear failed transaction. |

| Security | Login risk, device change, MFA, recovery, session events. | Account takeover investigation lacks evidence. |

| Release | Approval, test results, feature flag, rollback state. | Production issue cannot be tied to a release. |

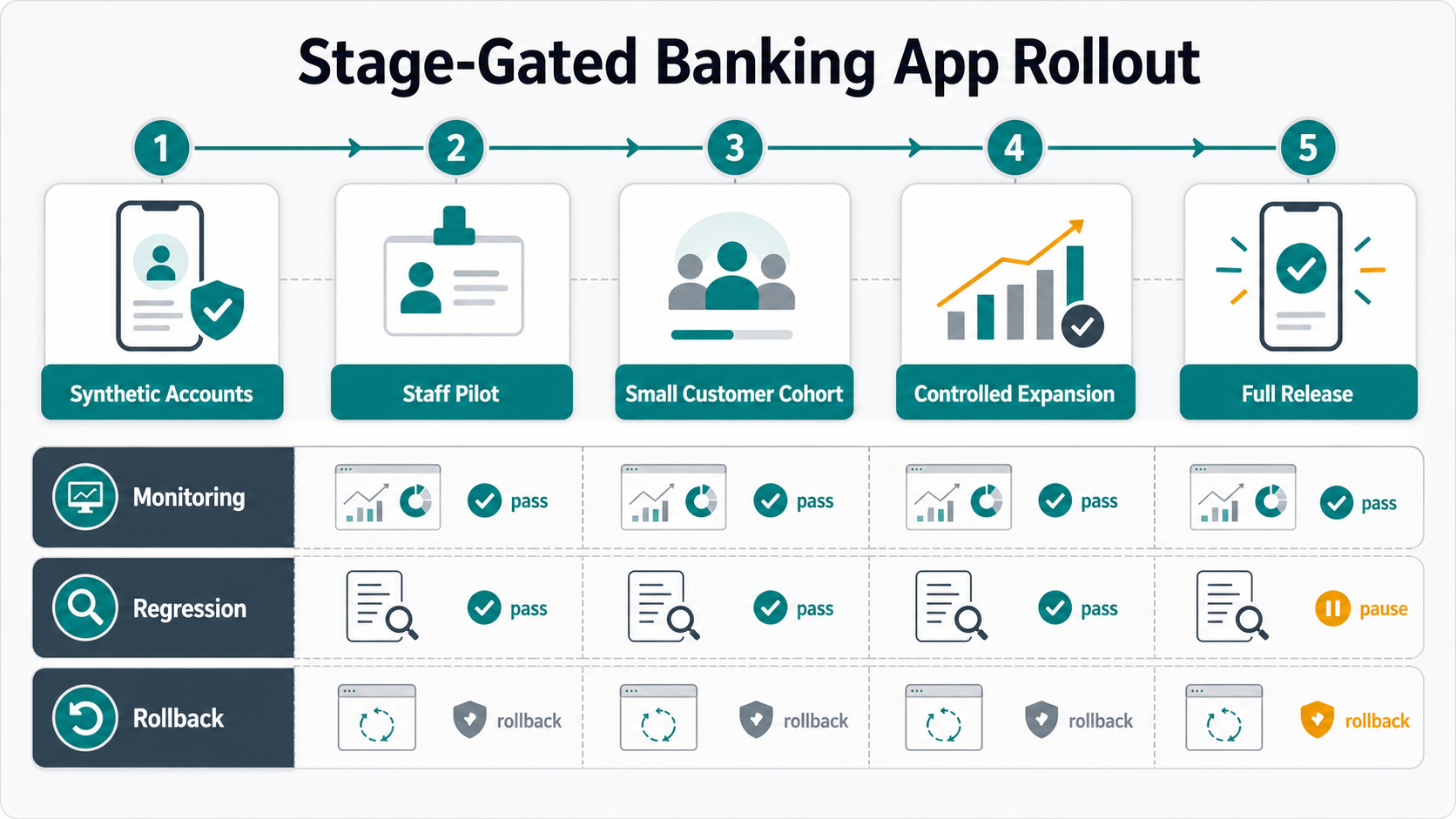

Use A Stage-Gated Rollout Instead Of A Big Reveal

Modernization should roll out in controlled waves. Start with internal testing and synthetic accounts, then staff pilots, then a small customer beta, then cohort expansion by app version, geography, customer type, or feature flag. Monitor login success, transaction completion, support contacts, crash-free sessions, API errors, fraud flags, customer feedback, and rollback readiness at each stage.

A strong release gate asks whether the app can proceed, pause, narrow, or roll back. Do not treat app-store submission as the finish line. The first production cohort is where real device diversity, network variability, user behavior, and backend data quality become visible.

If the modernization scope includes new workflow software, dashboards, admin tools, or support consoles, use custom software development to keep the mobile app and operational tooling aligned.

Roadmap Checklist

- Map current app risk by journey, system dependency, support issue, and compliance evidence gap.

- Stabilize identity, authentication, account recovery, device risk, and fraud signals before adding high-risk features.

- Define API contracts around customer journeys with latency, idempotency, audit, and fallback behavior.

- Redesign onboarding, balances, transfers, card controls, support, and statements with accessibility checks.

- Build consent, KYC, AML, payment, security, and release evidence into the product workflow.

- Run regression, security, API, device, network, and accessibility testing before each rollout wave, including penetration testing checklist coverage for web, API, admin, and mobile-adjacent surfaces.

- Use feature flags, cohorts, monitoring, and rollback procedures for every major release.

How NextPage Can Help

NextPage helps financial product teams modernize mobile banking apps through app assessment, architecture planning, secure UX, API modernization, testing strategy, workflow software, and staged rollout support. A practical engagement starts by identifying the highest-risk journeys and the backend constraints behind them.

From there, the roadmap can define the first modernization wave: identity and recovery, API gateway work, onboarding/KYC upgrade, transfer and payment resilience, card controls, support workflows, accessibility remediation, or release testing. If the current stack includes a legacy hybrid shell, the legacy hybrid mobile app modernization guide can help decide whether to maintain, migrate, or rebuild. The work should be small enough to ship safely and structured enough to improve trust with every release.